Table of Contents >> Show >> Hide

- Inflation in plain English: the “same dollars, smaller groceries” problem

- Housing is two things at once: an asset and a contract

- 5 reasons housing can hedge inflation (without pretending it’s invincible)

- 1) Replacement costs rise, and home prices often follow

- 2) Rents rise with inflationand shelter inflation is a major force

- 3) Fixed-rate mortgages can turn inflation into a discount (on your debt)

- 4) Housing gives you a built-in “forced savings” mechanism

- 5) Supply frictions can make housing resilient

- A quick “inflation math” example (no PhD required)

- Important reality check: housing is not a perfect inflation hedge

- Homeownership vs. rentals vs. REITs: “housing” is not one single thing

- How to use housing as an inflation hedge without turning it into a horror movie

- So… is housing a good inflation hedge?

- Experiences and real-world lessons about housing as an inflation hedge (extra depth)

- Experience #1: The homeowner who locked a low fixed rate feels the contrast immediately

- Experience #2: The renter who delays buying discovers that inflation can raise the entry price

- Experience #3: The landlord learns inflation hedges have expenses too

- Experience #4: The homeowner in a high-risk area learns the insurance line item is not a rounding error

- Experience #5: The “hedge” shows up as lifestyle flexibility, not just dollars

- Conclusion

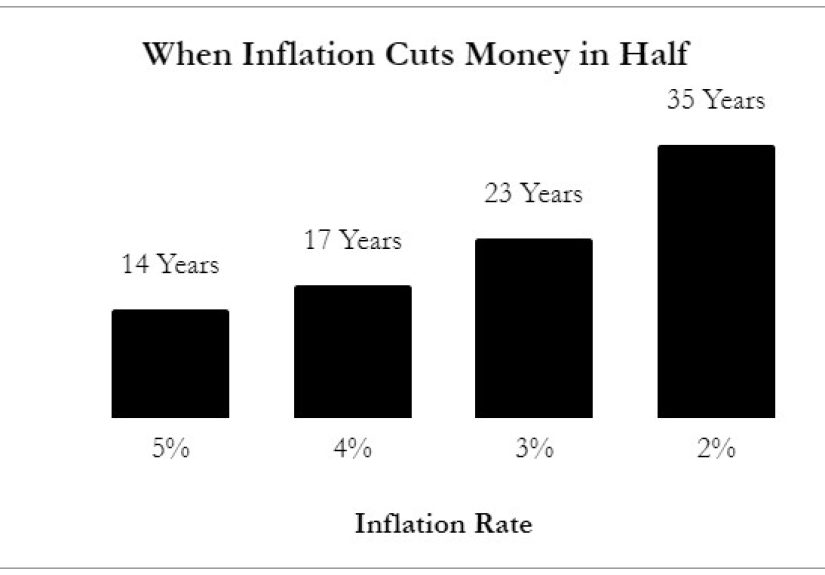

Inflation is basically the universe’s way of saying, “Congrats on saving moneynow watch it buy less stuff.”

It’s not always a headline-grabbing monster, but even “normal” inflation quietly gnaws at your purchasing power.

That’s why so many people go hunting for inflation hedges like they’re trying to outrun a raccoon that just stole their sandwich.

One of the simplest, most “regular-person” hedges is also the biggest purchase most Americans ever make: a home.

And the idea behind A Wealth of Common Sense’s take is refreshingly practical: housing can hedge inflation not because it’s magical,

but because it combines a real asset with a long-term fixed payment planand inflation tends to play favorites with that combination.

Inflation in plain English: the “same dollars, smaller groceries” problem

Inflation means prices rise over time and money loses purchasing power. You don’t notice it day-to-day as much as you do year-to-year:

the fast-food meal that used to cost $8 now costs “please don’t look at the receipt.”

Over long stretches, inflation can cut the real value of cash dramaticallywhich is why long-term savers care so much.

The tricky part is that inflation hits your life through the biggest budget categories: food, energy, and especially shelter.

“Shelter” is a huge component of inflation measures because housing costs are a huge part of what households spend.

Housing is two things at once: an asset and a contract

A home isn’t just a roofit’s also a long-term financial structure. When you buy, you’re usually doing three things at the same time:

- Owning a real asset (land + structure) that tends to reprice over time.

- Locking in housing consumption (you live there, and you’re not renegotiating your “rent” every year).

- Financing it with long-term debtoften a 30-year fixed-rate mortgage.

That last point is where inflation can get oddly helpful. Inflation is bad for people holding lots of cash,

but it can be good for people repaying long-term fixed debts with future dollars that are worth less. That’s the “quiet superpower”

of owning housing with a fixed-rate mortgage.

5 reasons housing can hedge inflation (without pretending it’s invincible)

1) Replacement costs rise, and home prices often follow

When inflation shows up, it doesn’t just hit lattes. It hits lumber, concrete, appliances, contractor labor, and permits.

As replacement costs rise, the value of existing housing can rise toobecause building a new “equivalent” home gets more expensive.

Over long periods, broad home price measures track how the market reprices housing as costs and incomes change.

2) Rents rise with inflationand shelter inflation is a major force

In many places, rents tend to increase over time, especially when wage growth and general price levels are rising.

That matters even if you’re a homeowner, because homeownership implicitly replaces what would have been rent payments.

In inflation statistics, rent and owners’ equivalent rent (OER) are core ways shelter costs are measured.

Also, shelter inflation measures often move with a lag relative to “market rent” changes, because leases are sticky and renewals are smoothed.

In other words: rents can jump in the real world, and the official numbers might catch up later.

3) Fixed-rate mortgages can turn inflation into a discount (on your debt)

Here’s the cleanest way to see it: if you lock in a fixed mortgage payment, your monthly principal-and-interest payment is nominally stable.

Inflation and income growth can make that fixed payment feel smaller over time.

Your mortgage doesn’t automatically go up just because everything else did.

And in the U.S., the 30-year fixed-rate mortgage is a common productmeaning many homeowners can “freeze” the financing cost for decades.

Mortgage rates move around with broader interest rates and market expectations, but once you lock a fixed rate, your payment is your payment.

4) Housing gives you a built-in “forced savings” mechanism

Homeownership often forces disciplined behavior. Every payment (especially early on) includes interest, but also typically includes principal.

That principal paydown is a form of savings that renters don’t get automatically.

In an inflationary environment, “forced savings into a real asset” can matter because the alternativeletting cash sitoften loses real value.

5) Supply frictions can make housing resilient

Housing supply doesn’t adjust instantly. Zoning, land constraints, permitting timelines, and the sheer time it takes to build

can keep supply tight even when demand changes.

Research commentary has pointed out how U.S. housing price dynamics can be surprisingly resilient compared with some other countries,

especially when market structures and financing differ.

A quick “inflation math” example (no PhD required)

Imagine you buy a home with a 30-year fixed mortgage where the principal-and-interest payment is $2,000/month.

Now assume inflation averages 3% annually and your household income trends up over time with the economy.

- Year 1: $2,000 feels like $2,000 (rude).

- Year 10: after cumulative inflation, $2,000 has less purchasing power than it did in year 1.

- Year 20: that same $2,000 can feel even smaller relative to wages and general prices (assuming income growth keeps pace).

Meanwhile, if you were renting, your landlord would likely attempt to reprice the rent periodically toward prevailing market conditions.

Not always smoothly. Not always fairly. But rent resets are common; mortgage payments don’t reset the same way.

Important reality check: housing is not a perfect inflation hedge

If housing were a flawless hedge, we’d all buy three houses and ride into the sunset on a lawnmower made of gold.

In real life, housing has trade-offsand inflation can raise your costs too.

Costs that can inflate faster than you want

- Property taxes can rise with assessed values and local budgets.

- Insurance can spike in riskier regions (and has been a growing affordability pressure in many markets).

- Maintenance and repairs get more expensive when labor and materials inflate.

Interest rates can change the game (especially for new buyers)

Higher mortgage rates can crush affordability, and that can slow price growth or cause drawdowns in certain markets.

If you’re buying today, your “hedge” depends heavily on the price you pay and the rate you lock in.

Affordability measures and market reports often highlight how rates influence who can buy and how much home they can afford.

Housing is local, illiquid, and occasionally dramatic

Housing markets are famously local. A booming metro area can do great while another region stagnates.

And selling a house isn’t like selling a stockyou can’t click “Sell” and be done before lunch.

Also: home prices can fall, sometimes sharply. Broad indexes like Case-Shiller show how cycles can produce painful declines.

Homeownership vs. rentals vs. REITs: “housing” is not one single thing

Your primary home

A primary residence is part investment, part lifestyle choice. Its “return” includes something you don’t see on a brokerage statement:

you’re consuming housing services (shelter) without paying a landlord for them. That’s a big deal when rents rise.

Rental property

Rentals can hedge inflation through rent increases, but it’s not automatic. Leases, local laws, tenant turnover, vacancy,

and maintenance costs all matter. The upside is that rents can adjust upward over time; the downside is that your expenses can too.

(Inflation has no loyalty.)

REITs and housing exposure in public markets

Publicly traded real estate can provide real estate exposure with liquidity, but it behaves more like stocks day-to-day.

That can be good (easy to rebalance) and also annoying (volatility) depending on your goal.

How to use housing as an inflation hedge without turning it into a horror movie

If inflation protection is part of your motivation, the most important moves are boringbecause boring is where money survives.

Prioritize payment stability

- Fixed-rate financing is often the cleanest “inflation hedge” feature of homeownership.

- Avoid stretching so far that one surprise expense turns your hedge into a hedge maze.

Budget for the unsexy stuff

- Maintenance reserve (homes are adorable until the water heater auditions for a disaster film).

- Insurance shopping and reviews, especially in high-risk areas.

- Tax planning: understand what’s deductible and what isn’t.

Know the tax rules (but don’t buy a house “for the deduction”)

Some homeowners may be able to deduct mortgage interest if they itemize and meet the rules, but it’s not universal

and depends on your situation. Treat tax benefits as a potential bonus, not the foundation of the decision.

So… is housing a good inflation hedge?

Housing can be a strong hedge against inflation because it often combines:

(1) a real asset that can reprice over time,

(2) rent-linked shelter value, and

(3) long-term fixed-rate debt that inflation can quietly erode in real terms.

That combination is powerfuland it’s exactly why housing plays such a central role in household finances.

But it’s not automatic wealth. It’s a tool. A hammer can build a house or smash your thumbboth outcomes are technically “consistent with physics.”

The inflation-hedge story works best when the purchase price is reasonable, the financing is stable, and you’re prepared for the ongoing costs.

Experiences and real-world lessons about housing as an inflation hedge (extra depth)

To make this practical, here are several “real life” patterns that tend to show up when inflation runs hot. These aren’t personal anecdotes

(I don’t own a house, or a toolbox, or even a respectable collection of paint swatches). Instead, think of these as common experiences

pulled from how households, landlords, and buyers typically describe the trade-offs.

Experience #1: The homeowner who locked a low fixed rate feels the contrast immediately

A common story goes like this: someone buys a starter home, locks a fixed-rate mortgage, and then inflation rises.

Their friends who rent start seeing meaningful rent increases at renewal time, but the homeowner’s principal-and-interest payment barely moves.

The homeowner still complains (because everyone complains), but the complaint is different:

it’s about rising groceries and utilitiesnot a housing payment that suddenly jumped by $300 a month.

The lesson: the “hedge” isn’t only home price appreciation; it’s the stability of the payment stream.

Even when home prices flatten, having a predictable payment can protect cash flow and reduce stress.

That stability can be worth a lot when everything else feels like it’s repricing weekly.

Experience #2: The renter who delays buying discovers that inflation can raise the entry price

Another common experience: someone plans to buy “next year” after saving a bit more.

But inflation and higher construction/financing costs can make the target home more expensive,

and mortgage rates can change affordability faster than most people expect.

The buyer feels like they’re running up an escalator that’s going down.

The lesson: waiting can be smart, but it has a cost. Inflation can raise both the purchase price and the carrying costs.

This doesn’t mean “buy at any price.” It means be honest about the risk of postponing when inflation is elevated:

you might save more cash, but the goalposts might move.

Experience #3: The landlord learns inflation hedges have expenses too

Rental owners often find that rent can rise, but so can everything else:

repairs, contractor labor, property management fees, taxes, insurance, and compliance costs.

In some markets, raising rent is constrained by competition or tenant turnover risk.

In others, it’s constrained by regulation or by the reality that tenants can only pay what tenants can pay.

The lesson: real estate can hedge inflation, but cash-flow math matters more than slogans.

Landlords who budget for maintenance, keep reserves, and avoid excessive leverage tend to experience the hedge as “sturdy.”

Those who run thin margins can experience the same inflationary period as “expensive panic with a side of plumbing.”

Experience #4: The homeowner in a high-risk area learns the insurance line item is not a rounding error

Homeowners in regions exposed to storms, wildfires, or flooding sometimes face big premium jumps or coverage changes.

This can be a shock because the mortgage payment feels fixed and safe, but the total monthly housing cost

(mortgage + taxes + insurance) is what actually matters.

The lesson: the best inflation-hedge version of homeownership is the one that plans for non-mortgage costs.

When people say, “My payment is fixed,” the fine print is:

“My mortgage is fixed, but my taxes, insurance, and maintenance are very much alive.”

Buyers who price these realities in from day one usually feel more protected in inflationary periods.

Experience #5: The “hedge” shows up as lifestyle flexibility, not just dollars

A subtle experience many homeowners describe is that housing stability changes decision-making.

When inflation is high, a stable housing payment can make it easier to keep investing, keep saving,

or handle a job transition without feeling like your rent is about to reprice you out of your own life.

This isn’t a spreadsheet returnbut it’s a real benefit that can improve financial resilience.

The lesson: a good hedge isn’t only what goes up in price. It’s what prevents your budget from getting ambushed.

Housing can do thatespecially with stable financing and a realistic plan for the ongoing costs.

Conclusion

Housing can be a good hedge against inflation because it’s one of the rare mainstream assets that blends a real, useful thing (shelter)

with a long-term financing structure that inflation can quietly erode in your favor.

Add in the tendency for rents and replacement costs to rise over time, and it’s easy to see why homeowners often feel better protected

during inflationary stretches.

The smart approach is not “housing always wins.” It’s: buy a home you can afford, lock stable financing when possible,

plan for taxes/insurance/maintenance, and treat housing as a long-term toolnot a short-term trade.

Do that, and housing has a strong chance of acting like the steady, practical inflation hedge it’s famous for.