Table of Contents >> Show >> Hide

- Why Everyone Wants to Call the Top (and Why That’s Usually a Trap)

- The Big Idea: Most Days Are “The Middle”

- What “A Wealth of Common Sense” History Says About All-Time Highs and Drawdowns

- Market Timing: Even the Perfect Timer Isn’t the Hero in This Story

- Missing the Best Days: The Sneaky Cost of Trying to Dodge the Worst Ones

- The Behavioral Gap: It’s Not Just MarketsIt’s What We Do During Markets

- Tops, Bottoms, Middles: A Practical Playbook That Doesn’t Require a Crystal Ball

- Specific Example: A Late-30s Investor in a “Middling” Market

- Conclusion: Common Sense Isn’t Predicting the FutureIt’s Surviving It

- : Common Investing Experiences From the Middle of the Market

- Experience #1: “I knew it was the top… until it wasn’t.”

- Experience #2: “I got out to feel safe, then I couldn’t get back in.”

- Experience #3: “The middle made me restless.”

- Experience #4: “Diversification felt dumb… right up until it felt brilliant.”

- Experience #5: “My best decision was the one I didn’t make.”

If investing had a soundtrack, it wouldn’t be dramatic battle music 24/7. It would be 10 minutes of panic,

10 minutes of victory laps, and about 47 hours of elevator music called “The Middle.”

That’s the point behind the “tops, bottoms, and middles” idea popularized by Ben Carlson at

A Wealth of Common Sense: most of the time, the market isn’t handing out cinematic, once-in-a-generation

“BUY NOW!” or “SELL EVERYTHING!” moments. Most of the time, it’s just doing what markets domoving,

wobbling, frustrating everyone, and quietly rewarding patience.

This article is a practical, common-sense guide to understanding stock market tops, bottoms, and (yes)

the endlessly underrated middle. We’ll look at why calling tops and bottoms is so tempting, why it’s so hard,

what history says about all-time highs and drawdowns, and how to build an approach that doesn’t require

you to predict the future (because, inconveniently, none of us can).

Why Everyone Wants to Call the Top (and Why That’s Usually a Trap)

Market tops and bottoms are irresistible because they promise certainty. If you could sell at the top and buy at the bottom,

investing would be less like “disciplined long-term planning” and more like “press button, receive yacht.”

The problem is that tops and bottoms are obvious only in the rearview mirror. In real time, they look like noise,

narratives, and headlines screaming in ALL CAPS. When prices fall, it feels like the world is ending. When prices rise,

it feels like the world has been saved by your geniusuntil it dips again and your genius needs a nap.

The most common investor mistake isn’t a lack of intelligence. It’s a very human combo:

fear + urgency + a story that sounds smart. Add a hot take on social media and suddenly “staying the course”

sounds boring, while “I’m waiting for the real bottom” sounds brave.

The market doesn’t reward dramait rewards endurance

The irony: the more you try to avoid discomfort by hopping in and out, the more likely you are to miss the very returns

you’re chasing. Not because you’re “bad at investing,” but because market timing requires repeated, near-perfect

decisions in unpredictable conditions.

The Big Idea: Most Days Are “The Middle”

Here’s a reality check that feels mildly offensive the first time you accept it:

most investing years are not peak years or crisis years. They’re muddle-through years. Sideways years.

“My portfolio is doing… something” years.

Carlson’s framing is helpful because it gives you permission to stop acting like every month should contain a

life-changing entry or exit point. Market cycles do have tops and bottoms. But the “middle” is where you

actually live as an investormaking contributions, rebalancing, ignoring noise, and occasionally Googling

“is this a recession?” at 1:00 a.m.

What “A Wealth of Common Sense” History Says About All-Time Highs and Drawdowns

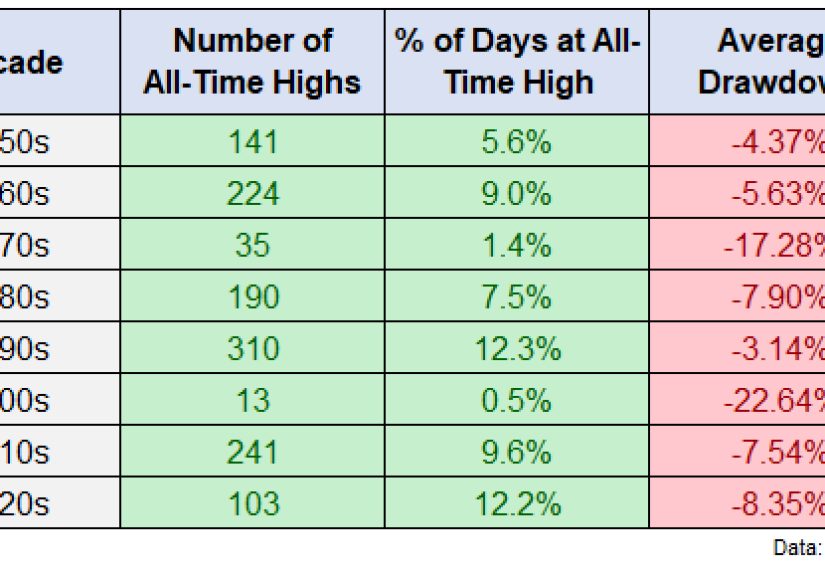

One of the most useful takeaways from Carlson’s research is that new all-time highs are meaningfulbut they’re not constant.

Depending on the decade, the market may set lots of new highs… or very few. Either way, investors still have to deal with

drawdowns along the way.

He highlights a few counterintuitive facts:

-

All-time highs don’t happen every week. Some decades have plenty; others are stingy.

That doesn’t mean “the market is broken.” It means markets move in regimes. -

Drawdowns are normal. Even when the long-term trend is up, the market spends a lot of time below its prior peak.

That’s not a bugit’s the admission price. -

The middle can be mentally harder than the bottom. At least bottoms feel like a “moment.”

The middle feels like waiting in line while someone ahead of you argues about coupons.

The “sideways” decade still moved (and still rewarded diversification)

People love to warn about a “1970s-style market” where stocks go sideways for years. That fear is understandable,

especially when inflation is high and headlines are loud. But the historical lesson is more nuanced:

even in weaker market decades, stocks can still produce positive nominal returnswhile inflation may reduce what

those returns feel like in real purchasing power.

The practical takeaway isn’t “panic.” It’s “plan.” If inflation is a risk, build a portfolio and savings strategy that

acknowledges itdiversify, keep contributing, and focus on the part you can control: behavior, costs, and time horizon.

Market Timing: Even the Perfect Timer Isn’t the Hero in This Story

If you’ve ever thought, “I’ll invest once things calm down,” congratulationsyou’re a normal mammal with a nervous system.

Unfortunately, the market has never signed a peace treaty with anyone’s nervous system.

One well-known Charles Schwab analysis makes the point with fictional investors:

even a “perfect” market timer doesn’t beat an immediate investor by some magical, life-altering amount.

Meanwhile, the person who waits in cash for the “right time” can fall dramatically behind.

Translation: procrastination can be more expensive than imperfect timing. Waiting feels safe, but it can quietly

become a long-term strategy of missing opportunities.

Dollar-cost averaging: the peace treaty between logic and feelings

If lump-sum investing makes your stomach do gymnastics, a consistent schedule can help:

invest the same amount weekly or monthly (like a 401(k) contribution), regardless of headlines.

It doesn’t guarantee profits, but it does reduce the temptation to “make the perfect call.”

In plain English: dollar-cost averaging can keep you from turning investing into an emotional improv show.

Missing the Best Days: The Sneaky Cost of Trying to Dodge the Worst Ones

This is the classic market-timing boomerang: you sell to avoid pain, but the market rebounds fastoften when confidence

is at its lowest. Many of the strongest single days occur near the worst periods because volatility cuts both ways.

Multiple major firms have published versions of the same lesson:

missing just a handful of the market’s best days can meaningfully reduce long-term results.

Fidelity, for example, shows how missing a small number of top days over decades can shrink outcomes dramatically.

Vanguard and Schwab show similar patterns over long periods.

Why this happens (and why it’s so annoying)

-

Big down days and big up days often cluster together. If you’re out of the market to “avoid volatility,”

you can miss the snapback. -

Re-entries are hard. People don’t usually buy back in because they feel bravethey buy back in when things feel

“safe,” which can be after a lot of the rebound. - Timing requires two correct decisions. You need a good exit and a good re-entry. Getting one right isn’t enough.

The Behavioral Gap: It’s Not Just MarketsIt’s What We Do During Markets

Even if you buy solid funds, diversify, and keep costs reasonable, your returns aren’t only driven by the market.

They’re also driven by your timing of contributions and withdrawalsand by whether you panic-sell during drawdowns.

Research firms that study investor behavior (including DALBAR and Morningstar) repeatedly highlight a frustrating pattern:

the “average investor” often earns less than the investments they own because they buy and sell at unhelpful times.

In other words, people tend to chase performance and flee discomfortexactly backward.

The goal isn’t to be emotionless. The goal is to design a system that works even when you feel emotional.

Tops, Bottoms, Middles: A Practical Playbook That Doesn’t Require a Crystal Ball

Here’s the common-sense approach that holds up across market cycleswhether we’re near a top, a bottom, or stuck in the middle

like a sitcom character who can’t find the exit door.

1) Start with one question: “When do I need the money?”

If you need the money next year, it shouldn’t be in a volatile stock-heavy portfolio. If you need the money in 20–30 years,

short-term volatility is the price you pay for long-term growth potential.

This time-horizon lens is the antidote to obsession over tops and bottoms.

2) Pick an asset allocation you can actually stick with

The “best” portfolio on paper is useless if it causes you to bail at the worst time. Many investors do better with a slightly

more conservative mix that they can hold through ugly markets than with an aggressive mix that makes them panic.

3) Automate contributions so the middle doesn’t sabotage you

The middle is where boredom becomes risk. When nothing dramatic is happening, people start “tinkering.”

Automating contributions turns investing into a routine instead of a referendum on your mood.

4) Rebalance like an adult (not like a fortune teller)

Rebalancing is a disciplined way to “buy low and sell high” without pretending you can predict markets.

When stocks run hot, you trim back to target. When they fall, you add back to target.

It’s not glamorousso it works.

5) Build a “bad headlines” protocol

Decide in advance what you will do during a correction or bear market. Examples:

- Keep contributing on schedule.

- Rebalance quarterly or annually, not daily.

- Check your portfolio less often when volatility spikes.

- Keep an emergency fund so you’re not forced to sell at a bad time.

Specific Example: A Late-30s Investor in a “Middling” Market

Imagine an investor in their late 30s who plans to work another 25–30 years. They’ve been through a fast crash, a fast rebound,

a hot bull run, and a nasty bear market. Now the market feels stuckneither terrible nor thrilling.

The common-sense move is not to “wait for clarity.” It’s to:

- Keep monthly contributions rolling.

- Maintain a diversified portfolio (not a single-theme bet).

- Use the middle period to improve habits: emergency savings, debt management, and consistent investing.

- Rebalance, instead of chasing the latest winner.

Over decades, the investor’s future portfolio is shaped more by contributions made during uncertain periods than by a heroic

one-time purchase at “the bottom.”

Conclusion: Common Sense Isn’t Predicting the FutureIt’s Surviving It

Stock market tops and bottoms get the spotlight, but “the middle” is where long-term wealth is usually built.

Most days won’t feel like an obvious bargain or an obvious bubble. They’ll feel ordinary, noisy, and mildly inconvenient.

The winning strategy for most people is not perfect timing. It’s a resilient plan:

diversify, keep costs low, invest consistently, rebalance occasionally, and match risk to your time horizon.

That’s not excitingbut it’s what tends to work when markets refuse to cooperate with your feelings.

Important: This article is for educational purposes only and isn’t personal financial advice.

Consider your goals, time horizon, and risk toleranceor talk to a qualified professionalbefore making investment decisions.

: Common Investing Experiences From the Middle of the Market

I can’t claim personal investing memories, but I can share the kinds of experiences that show up over and over in

real-world investor storiespatterns that advisers, brokerages, and behavioral research frequently describe.

Think of these as “composite” experiences: not one person, but many familiar moments rolled into a few scenes.

Experience #1: “I knew it was the top… until it wasn’t.”

A lot of investors remember the first time they felt certain. Prices were soaring, friends were bragging, and the news

made it sound like the market had discovered a cheat code. Selling felt smartuntil the market kept rising and they watched

from the sidelines, waiting for a dip that didn’t arrive on schedule. The lesson isn’t that selling is always wrong.

It’s that certainty is expensive, and markets can stay irrational longer than your patience budget allows.

Experience #2: “I got out to feel safe, then I couldn’t get back in.”

This is the classic trap: selling during a scary stretch brings immediate emotional relief. But then the investor faces a new

fearbuying back in. If the market rises, it feels “too late.” If it falls again, it feels like the fear was justified.

So they wait. And wait. Eventually, they re-enter when headlines improvewhich often means after a meaningful portion of the

rebound has already happened. This isn’t a character flaw; it’s how loss aversion works in the human brain.

Experience #3: “The middle made me restless.”

The middle is weirdly dangerous because it’s boring. No emergency. No euphoria. Just choppy, sideways movement and

endless opinions. That’s when investors start “improving” their portfolios: swapping funds, chasing last year’s winner,

or hoarding cash for the perfect moment. In practice, this often raises costs, taxes, and regret without reliably improving

outcomes. The investors who do best in the middle usually do the least: contribute consistently, rebalance calmly, and go live

their lives.

Experience #4: “Diversification felt dumb… right up until it felt brilliant.”

Diversification is the broccoli of investing: you rarely crave it, but it’s good for you. When one sector is on fire,

a diversified portfolio can feel “behind.” Then leadership changesoften suddenlyand diversification becomes the reason

an investor avoids catastrophic overexposure. The emotional challenge is accepting that diversification is designed to keep you

in the game, not to win every short-term popularity contest.

Experience #5: “My best decision was the one I didn’t make.”

Many long-term investors eventually realize their best “move” was not a move at all: continuing contributions through

uncomfortable markets, keeping a sensible allocation, and refusing to negotiate with daily headlines. It’s not flashy.

But it’s common senseand common sense scales beautifully over decades.