Table of Contents >> Show >> Hide

- What Does “Diversifying Across Time” Actually Mean?

- Where Luck Comes In: The Sequence of Returns

- Dollar-Cost Averaging vs. Lump Sum: Which Helps With Timing Risk?

- What the Research Says About Time Diversification

- How Diversification Across Time and Assets Work Together

- Practical Ways to Beat (or at Least Tame) the Luck Factor

- Common Myths About Time Diversification and Luck

- Bringing It Back to “A Wealth of Common Sense”

- Real-World Experiences: How Time Diversification Plays Out

If you’ve ever opened your investment account and thought, “Did I offend the stock market in a past life?”welcome, you’ve met the luck factor.

The idea behind “the luck of the draw when diversifying across time” is simple but powerful: when you invest can matter almost as much as what you invest in. Some investors seem to be born under a bull-market star; others show up right before a crash. Same strategy, wildly different outcomes.

That sounds terrifying, but it doesn’t have to be. Time diversification, dollar-cost averaging, and smart asset allocation can take the edge off bad luck and make your long-term plan far more resilient.

What Does “Diversifying Across Time” Actually Mean?

When most people think of diversification, they picture different asset classesstocks, bonds, real estate, maybe a sprinkle of international funds to feel sophisticated. Time diversification approaches risk from another angle: instead of dumping all your money into the market on one date, you spread your investments over many dates.

In practice, this looks like:

- Contributing to your 401(k) every paycheck

- Setting a monthly automatic transfer into an index fund

- Investing bonuses or windfalls in chunks instead of one big bet

By investing regularly, you’re buying in at a mix of good times, bad times, and “meh” times. That’s time diversification: you diversify not only across assets, but across market environments. Academic work on time diversification shows that spreading risk over time can change the distribution of outcomes, even if the average long-term return of the stock market stays roughly the same.

Where Luck Comes In: The Sequence of Returns

The market doesn’t hand out returns in a neat, polite line. Some decades are amazing, some are mediocre, and some are basically a financial horror film. The order in which those good and bad years show up is called the sequence of returns.

Imagine two long-term investors:

- Ashley starts investing right before a long bull market. The first 10 years are stellar, the next 10 are flat.

- Blake invests the same amount, same portfolio, same total 20-year average returnbut Blake starts right before a nasty 10-year stretch, followed by a great decade.

On paper, the average annual return might look similar. In reality, Ashley’s portfolio probably looks much more impressive along the wayespecially if they’re not withdrawing money. That’s the “luck of the draw” in action.

It’s Even More Serious in Retirement

During your saving years, bad early returns can actually be a blessing: you’re buying more shares at cheaper prices. But once you start withdrawing, the logic flips. Now, poor returns early in retirementwhile you’re taking money outcan permanently damage your portfolio. This is called sequence-of-returns risk.

Studies and retirement-planning tools show that two retirees with identical savings and identical long-run average returns can end up with very different outcomes simply because one retires into a bull market while the other retires into a bear market. One portfolio might last 40 years; the other might run dry in 25. The “luck of the draw” isn’t just theoreticalit can decide whether you outlive your money or your money outlives you.

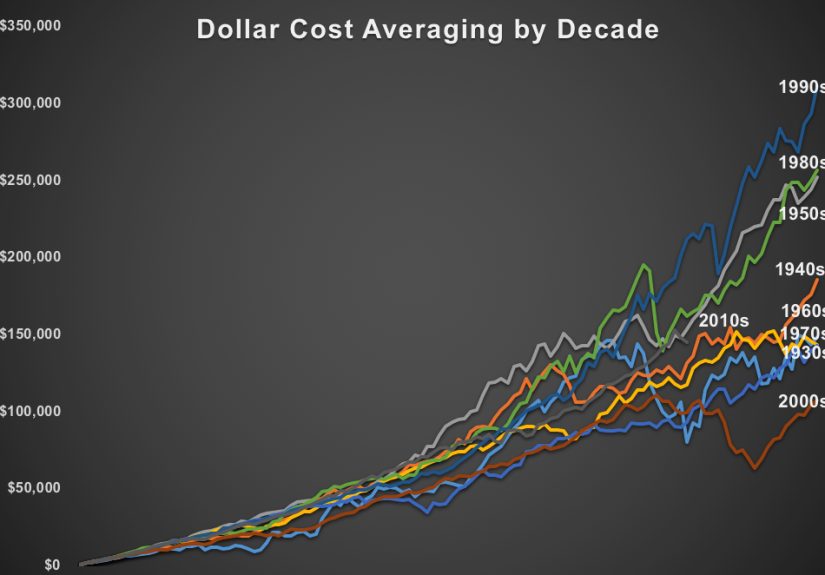

Dollar-Cost Averaging vs. Lump Sum: Which Helps With Timing Risk?

Any time we talk about time diversification, dollar-cost averaging (DCA) is going to crash the party.

Dollar-cost averaging means investing a fixed dollar amount at regular intervals, regardless of what the market is doing. You buy more shares when prices are low and fewer when prices are high. This is built into things like 401(k) contributions, and it’s a classic way to diversify across time.

Lump-sum investing is the opposite: you put a large amount of money into the market all at once. Historically, if you look at long periods during which markets trend upward, lump sum wins more often than notbecause your money has more time exposed to growth. Research from wealth-management firms and fund providers often shows lump sum outperforming DCA in 55–70% of historical scenarios over multi-year periods.

So is time diversification “worse” because DCA sometimes lags lump sum? Not necessarily.

- Mathematically, lump sum often wins in a rising market.

- Emotionally and behaviorally, DCA can be the difference between “I’m actually investing” and “I keep waiting for the perfect dip that never comes.”

- Risk-wise, DCA can soften the blow if your lump sum would otherwise land right before a major downturn.

A reasonable takeaway: lump sum may be “optimal” on average, but dollar-cost averaging is usually “more livable,” especially for nervous investors or those unlucky enough to invest near market peaks.

What the Research Says About Time Diversification

Economists have argued for decades about whether time truly diversifies risk or just feels like it does. Some papers show that as your time horizon lengthens, the probability of a negative total return on a diversified stock portfolio shrinkssuggesting that risk per unit of time may fall for long-term investors.

Other work counters that, while the chance of a loss might shrink, the range of possible outcomes grows. Over one year, your portfolio may swing between “mildly disappointing” and “pleasantly surprising.” Over 30 years, the gap between the unlucky cohort and the lucky cohort can be enormous. A recent survey of the time-diversification literature even called it a “puzzle,” noting that different assumptions about investor behavior, withdrawals, and risk preferences lead to very different answers.

In plain English: the longer your horizon, the more likely you are to come out ahead in stocks at all, but the more wildly your ending wealth can differ from someone who used the same strategy and just got a different market path. That’s the paradox of long-term investing.

How Diversification Across Time and Assets Work Together

Time diversification is powerful, but it’s not a solo act. You still need old-fashioned diversification across assets. Looking back over nearly a century of market history, researchers have shown that big stock drawdownsdrops of 20% or morehappen roughly once a decade and can take years to recover from. A portfolio that mixes stocks with bonds, cash, and other assets can significantly reduce the size and length of those drawdowns.

The combination of:

- Investing steadily over time (time diversification)

- Holding a globally diversified mix of stocks and bonds

- Rebalancing periodically to your target allocation

doesn’t eliminate luckbut it can make your results much less dependent on one specific moment in market history.

Practical Ways to Beat (or at Least Tame) the Luck Factor

1. Automate, automate, automate

Automating contributions is the most common real-life version of diversifying across time. You’re less likely to panic, second-guess yourself, or wait for the mythical “perfect entry point.” Your plan quietly buys during crashes, rallies, and sideways markets alike.

2. Match your risk to your timeline

Time diversification is not an excuse to be reckless. If you need the money in three years for a house down payment, the stock market is still a casino for that cash, no matter how brilliant your DCA spreadsheet looks. Long-term money (10+ years) can handle more stock exposure; short-term money belongs in safer, more liquid assets.

3. Keep a “sane-money” bucket

For retirees, one common strategy is the “bucket” approach:

- Short-term bucket: 1–3 years of living expenses in cash or cash-like investments.

- Medium-term bucket: a conservative mix of bonds and maybe some defensive stocks.

- Long-term bucket: growth assets like diversified stock funds that you don’t plan to touch for many years.

This doesn’t erase sequence-of-returns risk, but it gives you breathing room. If the market tanks early in retirement, you can draw mainly from the safer buckets while letting your long-term portfolio recover.

4. Rebalance instead of reacting

When markets soar, you may end up with more stocks than you intended. When markets crash, you may end up with far fewer. Rebalancingperiodically bringing your portfolio back to its target mixautomatically nudges you to buy low and sell high over time. It’s not glamorous, but it’s one of the cleanest ways to turn volatility from “scary” into “useful.”

Common Myths About Time Diversification and Luck

Myth 1: “Time always makes stocks safe.”

History shows that the longer you stay invested in a diversified stock portfolio, the less likely you are to end up with a loss. But “less likely” is not “impossible.” Markets have had long, painful stretches where even decade-long investors questioned their life choices. Time diversification tilts the odds in your favor; it doesn’t guarantee a win.

Myth 2: “If I start at the wrong time, I’m doomed.”

Starting at a terrible moment (say, right before a big crash) is frustratingbut not fatal if:

- You keep contributing

- You stay diversified

- You give your plan enough years to work

Many of the “worst-timed” investors in historythose who started just before major bear marketsstill ended up okay if they kept investing through the downturns instead of bailing out at the bottom.

Myth 3: “If lump sum usually wins, I should never DCA.”

Lump-sum investing often wins in spreadsheets where investors are robots with no feelings and no panic button. In real life, many people can only stomach investing a large amount if they break it into chunks. If DCA is what allows you to commit to a reasonable plan and stick to it, then it’s doing exactly what it’s supposed to dohelping you manage the luck of timing without freezing in place.

Bringing It Back to “A Wealth of Common Sense”

The phrase “a wealth of common sense” fits this topic perfectly. You don’t need exotic hedge funds or predictive AI models to deal with the luck of the draw. You need:

- A simple, diversified portfolio

- Regular contributions over many years

- A withdrawal strategy that respects sequence-of-returns risk

- The humility to accept that luck existsand the discipline to plan around it

Long-term investing will never be luck-free. But when you diversify across time and assets, you turn luck from the main character into a supporting role in your financial story.

Real-World Experiences: How Time Diversification Plays Out

Concepts are nice. But what does “the luck of the draw when diversifying across time” look like in real life? Let’s walk through a few composite stories that will feel uncomfortably familiar to a lot of people.

Case 1: The “Unlucky” Market-Timer Who Still Wins

Taylor graduated in the middle of a roaring bull market. Feeling brave (and armed with exactly three personal-finance blog posts), Taylor dumped a big signing bonus into a broad stock index fundright before a major correction.

Within months, that account was down 25%. Taylor felt like the poster child for bad luck. But there were two saving graces:

- Most of Taylor’s future contributions were still ahead.

- Contributions were automated every month, no matter what the headlines said.

Over the next decade, Taylor’s regular contributionsmade during the downturn and recoveryslowly turned that “horrible timing” story into a pretty normal long-term investing experience. The original lump sum looked rough for a while, but the steady DCA contributions bought shares at lower prices and helped bring the overall average cost down.

The lesson: terrible short-term timing doesn’t doom a young investor who keeps diversifying across time with regular contributions.

Case 2: The Near-Retiree Who Ignored Sequence Risk

Chris was 63, feeling great, and holding a very stock-heavy portfoliobecause “stocks always come back.” There was no cash bucket, no bond buffer, and no written plan for how to handle a bear market in retirement.

Two months after Chris retired, the market slid into a deep downturn. Worried about living expenses, Chris kept withdrawing the same dollar amount each montheven as the portfolio shrank. After two horrible years, the account balance was down far more than the market itself, because withdrawals had been taken at the worst possible time.

Had Chris set aside a few years of expenses in safer assets and diversified more thoughtfully, those withdrawals could have come from cash and bonds while the stock portion recovered. Instead, the luck of retiring into a bear market collided with a lack of time and asset diversificationand the damage was hard to undo.

Case 3: The Boring, Automated, Surprisingly Successful Saver

Jordan never tried to time the market; Jordan also never tried to predict interest rates, the Fed, inflation, or which sector would be hot next year. Instead:

- 10–15% of every paycheck went into a diversified mix of index funds.

- Contributions were increased after every raise.

- The portfolio was rebalanced once a year, almost on autopilot.

Over 25–30 years, Jordan lived through recessions, bubbles, inflation scares, political crises, and more than one scary headline about “the end of the 60/40 portfolio.” The account balance didn’t climb in a straight line, but it did climbsteadily, relentlessly, and surprisingly fast in the later years as compounding kicked in.

Did Jordan get lucky with starting dates? Maybe. But the bigger story is that by diversifying across time with regular investing, and across assets with a sensible allocation, Jordan made luck less decisive. Any given year mattered less because there were so many years in the plan.

What These Experiences Have in Common

Across all three cases, the key theme is not “how to beat luck,” but how to keep luck from running your entire financial life:

- Process over prediction: None of these investors could control returns, but they could control how and when they invested.

- Time on your side: Spreading contributions across many years made any single unlucky moment less catastrophic.

- Planning for bad sequences: Especially near and in retirement, having safer assets to draw from transformed a bad sequence of returns from a disaster into a rough patch.

The luck of the draw will always be there. But by diversifying across time, keeping your strategy simple, and respecting the realities of sequence risk, you give yourself something much more powerful than luck: a repeatable, common-sense process for building wealth over decades.