Table of Contents >> Show >> Hide

- Why the 2020 tax year confused so many people

- W-2 vs. 1099: what is the difference?

- The key W-2 and 1099 deadlines for 2020 taxes

- The big catch: the May 17, 2021 extension did not rewrite everything

- How to know whether a worker should get a W-2 or a 1099

- Important filing details employers and payers should not overlook

- What about extensions?

- What happens if you miss a W-2 or 1099 deadline?

- Common mistakes during 2020 reporting season

- 1. Using 1099-MISC for contractor pay instead of 1099-NEC

- 2. Assuming the May extension covered W-2 and 1099 deadlines

- 3. Waiting too long to collect W-9 information

- 4. Confusing employee reimbursement and contractor payment reporting

- 5. Forgetting the recipient deadline while focusing only on government filing

- Simple examples to make the deadlines easier

- Best practices for smoother future reporting seasons

- Conclusion

- Experiences from the 2020 reporting season

- SEO Tags

Tax deadlines have a special talent for showing up like an uninvited relative: suddenly, loudly, and right when you thought you had everything under control. If you were dealing with 2020 taxes, the confusion was even worse. Businesses were juggling payroll changes, pandemic disruptions, a brand-new 1099-NEC form, and the very reasonable question, “Wait, which deadline applies to me again?”

This guide breaks down the real deadlines for W-2 and 1099 tax reporting for 2020 taxes, explains the difference between the forms, and clears up one of the biggest misunderstandings from that year: the fact that the individual income tax deadline moved, but most W-2 and 1099 reporting deadlines did not. If you are writing for employers, bookkeepers, freelancers, or anyone trying to decode tax paperwork without needing a stress snack, you are in the right place.

Why the 2020 tax year confused so many people

The 2020 tax year was unusual for just about everyone. Employers were adapting to remote work, payroll departments were handling new reporting wrinkles, and many independent contractors had income that changed dramatically from quarter to quarter. Then came the calendar twist: although individual federal income tax returns for 2020 were later due on May 17, 2021, businesses still had much earlier deadlines for issuing wage and income statements.

That difference matters. If you were an employer, you could not look at the May tax filing extension and decide your W-2 or 1099 forms could take a leisurely spring vacation. Those forms still had to move fast.

W-2 vs. 1099: what is the difference?

Form W-2

A Form W-2 is used to report wages paid to employees. It shows taxable wages, Social Security wages, Medicare wages, and the taxes withheld during the year. In plain English, it is the tax world’s official receipt showing what an employee earned and what the employer already sent to the government.

Form 1099-NEC

For tax year 2020, the IRS brought back Form 1099-NEC to report nonemployee compensation. That means payments of $600 or more for services performed by someone who is not your employee, such as a freelancer, consultant, designer, or independent contractor. This was a major shift because many payers had previously reported contractor pay on Form 1099-MISC.

Form 1099-MISC

Form 1099-MISC still existed for tax year 2020, but it handled other types of reportable payments, such as rent, royalties, certain prizes and awards, medical and health care payments, crop insurance proceeds, and some attorney-related reporting. In other words, 1099-MISC did not retire. It simply stopped being the main stage for nonemployee compensation.

If you remember only one thing from this section, make it this: employees generally get W-2s; independent contractors generally get 1099-NEC forms. That one distinction prevents a shocking number of January headaches.

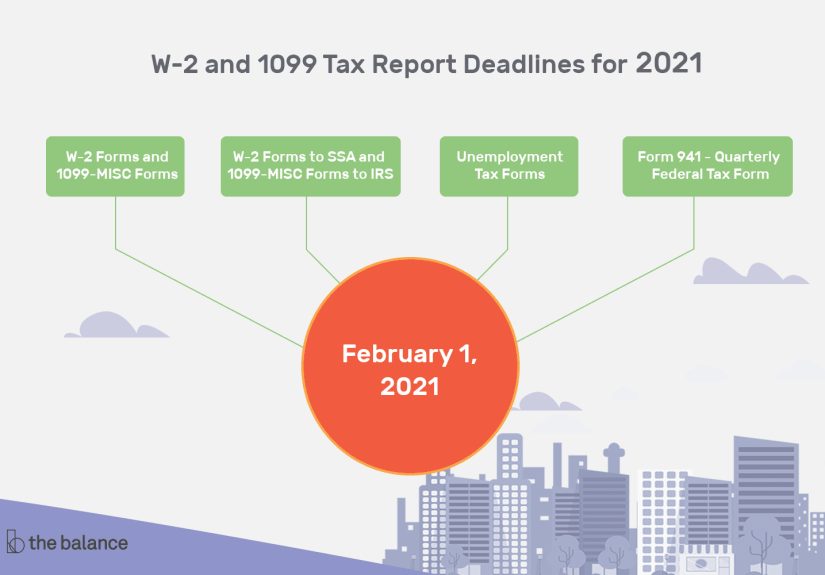

The key W-2 and 1099 deadlines for 2020 taxes

Here is the short version that most readers came for, probably while clutching coffee and searching frantically:

| Form | Recipient Deadline | Agency Filing Deadline | Notes |

|---|---|---|---|

| W-2 | February 1, 2021 | February 1, 2021 with the SSA | Same date for paper and electronic filing |

| 1099-NEC | February 1, 2021 | February 1, 2021 with the IRS | Used for nonemployee compensation |

| 1099-MISC | February 1, 2021 in most cases | March 1, 2021 on paper; March 31, 2021 electronically | If reporting only box 8 or 10 payments, recipient deadline was February 16, 2021 |

That table is the heart of the whole story. The 2020 tax year created plenty of noise, but the reporting calendar itself was not mysterious once you separated worker forms from individual tax returns.

The big catch: the May 17, 2021 extension did not rewrite everything

Many taxpayers heard that the federal tax deadline for 2020 returns moved from April 15, 2021, to May 17, 2021. That part was true. But it applied to individual federal income tax returns and payments, not to every tax form floating around in the universe.

That distinction is where people got tripped up. A sole proprietor might have thought, “My 1040 is due in May, so my contractor forms must be too.” Nice thought. Wrong thought. The IRS did not turn the whole filing system into an all-inclusive resort. Information returns such as W-2s and 1099s still followed their own deadlines.

So if you were an employer or payer in early 2021, you had to work on two timelines at once:

- Early February for W-2 and 1099-NEC reporting

- March for many 1099-MISC filings

- May 17, 2021 for individual federal income tax filing and payment for 2020 returns

That is not a typo. It is just tax season doing tax season things.

How to know whether a worker should get a W-2 or a 1099

The deadline is important, but classification is even more important. If you hand out the wrong form, meeting the deadline does not magically save you. A worker should generally receive a W-2 if the business controls not only the result of the work but also important details about how the work is done. A worker is more likely to receive a 1099-NEC if they operate independently, control their own methods, and are paid as a contractor rather than an employee.

For example, if your company hires a full-time office manager, sets the schedule, provides the equipment, and withholds taxes, that worker is usually a W-2 employee. If you hire a freelance web designer for a project, pay them for services, and they control how the work gets done, that is usually a 1099-NEC relationship.

Get the classification wrong and you may face more than a filing problem. You could wander into payroll tax trouble, worker classification disputes, and a conversation with your accountant that begins with a long, meaningful sigh.

Important filing details employers and payers should not overlook

W-2 forms go to the SSA, not the IRS

One easy detail to miss is that Forms W-2 are filed with the Social Security Administration, along with Form W-3 when filing on paper. Employers still need the IRS for payroll tax returns, of course, but the wage statement filing itself routes through the SSA.

1099-NEC and 1099-MISC go to the IRS

By contrast, 1099 forms are generally filed with the IRS. If filing on paper, a payer may also need Form 1096 as the transmittal. Electronic filing follows a different process and deadline pattern, especially for 1099-MISC.

Mailing by the due date can count as timely furnishing

For recipient copies, the rule is not always “must arrive by the due date.” In many cases, the requirement is satisfied if the form is properly addressed and mailed on or before the due date. That matters for businesses sending forms at the last minute, though relying on the postal service during crunch time is a bit like wearing flip-flops to a mountain hike: technically possible, but not the smartest plan.

What about extensions?

Extensions existed, but they were not a free-for-all.

For many information returns, Form 8809 could provide an automatic 30-day extension to file. However, there was an important exception: there was no automatic extension for W-2 forms or for 1099-NEC. W-2 extensions were limited and tied to extraordinary circumstances. So if a business assumed “I’ll just file an extension” for everything, that assumption could backfire quickly.

In practice, the smartest move was still the least glamorous one: gather worker information early, confirm names and taxpayer identification numbers, and prepare forms before the end-of-January stampede began.

What happens if you miss a W-2 or 1099 deadline?

The IRS can impose penalties for two separate failures:

- Failing to file correct information returns on time

- Failing to provide correct payee statements on time

That means being late can hurt twice. Send the form late to the worker or contractor? Problem. File the form late with the government? Also a problem. Send a form with incorrect information? Congratulations, tax season has unlocked a bonus level.

Late filings can also create practical trouble beyond penalties. Employees may not be able to file their tax returns accurately. Contractors may not know what income was reported under their taxpayer identification number. And if corrections are needed later, the cleanup often takes far more time than getting it right in the first place.

Common mistakes during 2020 reporting season

1. Using 1099-MISC for contractor pay instead of 1099-NEC

Tax year 2020 was the first year many businesses had to use the restored 1099-NEC. A lot of people were operating on muscle memory and almost reported nonemployee compensation on 1099-MISC out of habit.

2. Assuming the May extension covered W-2 and 1099 deadlines

It did not. The extension was for individual 2020 income tax returns and payments, not a broad pardon for every reporting deadline in sight.

3. Waiting too long to collect W-9 information

If you wait until late January to ask a contractor for a taxpayer identification number, you are inviting chaos to dinner. Businesses that collected Form W-9 information early usually had a much smoother reporting season.

4. Confusing employee reimbursement and contractor payment reporting

Some payments belong on payroll and a W-2. Others belong on 1099 forms. Treating them interchangeably is a classic compliance mistake.

5. Forgetting the recipient deadline while focusing only on government filing

It is not enough to file with the agency. Workers and payees must also receive their copies on time.

Simple examples to make the deadlines easier

Example 1: Small retail shop with employees

A retail shop had five employees in 2020. The owner needed to furnish each employee’s W-2 and file Copy A with the SSA by February 1, 2021.

Example 2: Marketing agency hiring freelance writers

A marketing agency paid three freelance writers more than $600 each in 2020. Those writers were nonemployees, so the agency needed to issue 1099-NEC forms to them and file those forms with the IRS by February 1, 2021.

Example 3: Landlord reporting rents and other miscellaneous payments

If a business had reportable miscellaneous payments that belonged on 1099-MISC, recipient copies were generally due by February 1, 2021, while filing with the IRS was due by March 1, 2021 on paper or March 31, 2021 electronically.

Best practices for smoother future reporting seasons

Even though this article focuses on W-2 and 1099 tax report deadlines for 2020 taxes, the practical lessons still hold up:

- Classify workers correctly from the start

- Collect Forms W-4 or W-9 before paying people

- Reconcile payroll records before year-end

- Confirm names, addresses, and taxpayer identification numbers early

- Do not assume income tax return extensions also move information return deadlines

- Use a checklist instead of trusting your January brain

A checklist may not be glamorous, but neither is paying avoidable penalties.

Conclusion

The most important thing to remember about W-2 and 1099 tax report deadlines for 2020 taxes is that the forms did not all move together. For tax year 2020, W-2s and 1099-NEC were generally due by February 1, 2021. 1099-MISC had a different schedule, with March 1, 2021 for paper filing and March 31, 2021 for electronic filing, while recipient copies were generally due earlier.

Meanwhile, the much-publicized May 17, 2021 deadline applied to individual federal income tax returns and payments for 2020, not to most employer wage statements or contractor reporting forms. Once you separate those categories, the calendar suddenly makes a lot more sense.

In short: know who is an employee, know who is a contractor, know which form belongs to which payment, and never let a tax deadline sneak up on you wearing sunglasses and pretending to be harmless.

Experiences from the 2020 reporting season

One of the most memorable things about the 2020 reporting season was how often smart, experienced business owners got tripped up by perfectly understandable assumptions. Many had heard nonstop coverage about delayed tax deadlines, stimulus payments, and shifting IRS procedures. So when January and February 2021 arrived, they naturally assumed all tax forms had been pushed back in the same way. That was not true, but it was a very human mistake.

Bookkeepers often described the season as a mix of urgency and confusion. Payroll records had to be finalized quickly, yet many companies were still adjusting to remote operations. Some teams no longer had their normal in-office year-end routines. Others were processing payroll changes caused by furloughs, reduced hours, hazard pay, or temporary staffing changes. It was not always the technical tax rules that caused the biggest problems. Sometimes the real issue was simply that the old workflow had disappeared.

The return of Form 1099-NEC added another layer. Businesses that had reported contractor payments on 1099-MISC for years suddenly had to switch forms. For tax professionals, this change made perfect sense. For busy owners handling ten different tasks at once, it felt like the government had rearranged the kitchen drawers overnight and expected everyone to cook dinner without looking. Plenty of businesses caught the issue in time. Others discovered it at exactly the wrong moment: when they were ready to print forms and realized the boxes did not match what they were trying to report.

Freelancers and independent contractors had their own version of the drama. Some were waiting on multiple forms from multiple clients, while also trying to understand whether the delayed May individual filing deadline changed what they needed to collect in January and February. It usually did not. The result was a lot of inbox checking, a lot of “just following up” emails, and a lot of people discovering that one client was wonderfully organized while another appeared to be navigating tax season with a blindfold and a dartboard.

For employees, the experience was often simpler but still stressful. Workers knew W-2 forms were coming, but mailing delays and remote HR processes sometimes made it feel as though the form had been sent by carrier pigeon. In many cases, the employer had technically furnished the W-2 on time by mailing it by the deadline, but employees still had to wait for delivery. That gap between “sent” and “received” created plenty of worry, especially for people eager to file early and claim refunds.

The biggest lesson from that season was not just “know the deadlines.” It was separate the deadlines in your mind. Information returns have one calendar. Individual returns have another. Worker classification has its own set of consequences. And if a year brings unusual IRS announcements, it is worth checking which forms are actually affected instead of assuming the entire tax system has been placed on one giant snooze button.

That experience still matters today because it shows how compliance problems usually begin: not with bad intentions, but with mixed signals, old habits, and one too many assumptions. The businesses that handled 2020 reporting best were usually the ones that slowed down, verified the rules, and treated each form as its own separate assignment. Not glamorous, no. Effective? Absolutely.