Table of Contents >> Show >> Hide

- The Short Thesis: Rising Rates Usually Create Pressure, Not an Automatic Collapse

- Why Rising Rates Can Hurt REITs

- Why Rising Rates Do Not Automatically Wreck REIT Performance

- What Recent Market History Says

- Which REITs Are More Vulnerable When Rates Rise?

- Which REITs May Hold Up Better?

- What Investors Should Watch Instead of Just Watching the Fed

- So, Will Rising Rates Hurt REIT Performance?

- Investor Experiences From a Rising-Rate REIT Cycle

- Conclusion

- SEO Tags

REIT investors have heard the same warning so many times it practically deserves its own theme music: Rates are rising, run for cover. It sounds dramatic, it makes for a tidy headline, and it is only half true. Yes, rising interest rates can hurt REIT performance. They can raise borrowing costs, pressure property values, and make dividend-paying real estate stocks look less dazzling next to safer income alternatives. But the real answer is messier, more interesting, and far more useful for investors.

REITs are not delicate flowers that wilt the second a Treasury yield twitches higher. They are operating businesses that own apartments, warehouses, shopping centers, cell towers, data centers, medical buildings, storage facilities, and a long list of other income-producing properties. That means performance depends on far more than one line on a Federal Reserve chart. The direction of rents, the health of tenants, the amount of new supply, the quality of management, and the structure of a REIT’s balance sheet all matter. Sometimes they matter a lot more than rates themselves.

So, will rising rates hurt REIT performance? The honest answer is this: they can, but they do not automatically doom the asset class. In some environments, REITs struggle. In others, they adapt just fine. And in the best cases, they surprise investors who expected them to behave like bond substitutes wearing expensive loafers.

The Short Thesis: Rising Rates Usually Create Pressure, Not an Automatic Collapse

When rates rise, REITs usually face three immediate challenges. First, debt becomes more expensive. Second, investors can suddenly earn more from bonds, cash, and other lower-risk assets, which reduces the relative appeal of REIT dividends. Third, higher discount rates can pull down property valuations, especially when investors are already nervous about economic growth.

That is the bearish case, and it is not imaginary. It is very real. But it is also incomplete.

REITs often perform worst when rates rise for bad reasons, such as sticky inflation, tightening financial conditions, weak growth, or recession fears. In that kind of environment, landlords can get squeezed from both sides: financing gets costlier while revenue growth slows. That combination is ugly. On the other hand, when rates rise because the economy is growing, employment is healthy, and space demand is improving, many REITs can offset the pressure through rent growth and stronger operating results.

In other words, it is not just the fact that rates are rising. It is why they are rising and which REITs are standing in the blast zone.

Why Rising Rates Can Hurt REITs

1. Borrowing costs go up

Real estate is a capital-intensive business. Buildings are expensive, land is not exactly a coupon-clipping hobby, and acquisitions often require debt or fresh equity. When interest rates climb, refinancing becomes more painful and new deals become harder to justify. A REIT that could once borrow cheaply to buy a property with an attractive spread may suddenly discover that the math no longer works. The deal that looked brilliant at 3% debt financing can start looking like a regrettable group project at 6%.

This matters even more for REITs that depend heavily on external growth. If a company constantly raises capital to buy more assets, rising rates can slow that machine down. Existing properties may still perform well, but the expansion engine can sputter.

2. Property values can face valuation pressure

Higher interest rates affect the valuation math behind real estate. Investors typically compare property income to financing costs and to available returns elsewhere in the market. When Treasurys and corporate bonds offer more yield, buyers often demand better pricing from real estate too. That can push cap rates higher and values lower, especially for assets with slower growth prospects.

This does not mean every building suddenly becomes worth less overnight. Real estate reprices slowly, unevenly, and often with a dramatic amount of denial along the way. Still, the pressure is real, especially in sectors already dealing with weak demand or heavy supply.

3. REIT dividends face tougher competition

REITs attract many income-focused investors. When short-term rates were near zero, a solid REIT dividend looked like a very attractive proposition. But when cash yields, CDs, or Treasury securities move higher, some investors decide they can collect income without taking equity risk. That relative shift can weigh on REIT share prices even if the underlying properties are still doing okay.

This is one reason REITs sometimes trade more like interest-rate-sensitive stocks than pure property companies. Market pricing can change fast, even when real estate fundamentals move slowly.

4. Mortgage REITs can be especially rate-sensitive

Not all REITs are built the same way. Equity REITs own properties. Mortgage REITs invest in real estate debt and mortgage-related securities. Because mortgage REITs often use more leverage and operate closer to the plumbing of interest rate spreads, they can be much more sensitive to rate shocks, funding conditions, and hedging effectiveness. So when investors ask whether rising rates hurt REITs, the first follow-up should be: Which kind?

Why Rising Rates Do Not Automatically Wreck REIT Performance

1. Rent growth can offset higher financing costs

If inflation is elevated and the economy remains reasonably healthy, many property owners can push rents higher. That is especially true in sectors with tight supply, strong tenant demand, or short lease durations that allow faster repricing. Self-storage, apartments, and some retail formats have historically had better flexibility here than sectors locked into long leases with limited pricing power.

This is the overlooked part of the REIT story. A company with rising net operating income, healthy occupancy, and disciplined capital allocation may absorb higher rates far better than investors assume. A rate increase hurts. A rent increase helps. The winner is whichever effect proves stronger.

2. The cause of higher rates matters

There is a major difference between “rates are rising because growth is strong” and “rates are rising because inflation is sticky and everyone is miserable.” The first scenario can support landlords through better leasing demand, higher occupancy, and stronger rent collections. The second is far more dangerous. It can create a stagflation-style environment where financing costs rise while growth fades. For REITs, that is the equivalent of getting hit by traffic from both directions.

3. Many public REITs are better capitalized than people think

One of the most persistent myths in the market is that all REITs are wildly overleveraged. Some certainly push harder on debt than others, but many listed REITs spent years extending debt maturities, locking in fixed-rate financing, and improving balance sheets. That does not make them immune to rising rates. It does mean the pain can arrive more gradually than people expect.

A REIT with mostly fixed-rate debt and limited near-term refinancing needs is in a very different position from one staring down a wall of maturities. Investors who lump them together are usually volunteering to miss the point.

4. Sector selection matters more than broad labels

The REIT market is not one giant monolith with matching cash flows and identical problems. It is a collection of subsectors that can move in very different directions. Recent market history has made that painfully obvious. Specialty REITs have at times outperformed sharply, while weaker areas such as office have continued to wrestle with structural issues. Rising rates do not hit every niche with the same force, and investors who buy “real estate” as if it were one single trade can end up owning very different realities under one ticker umbrella.

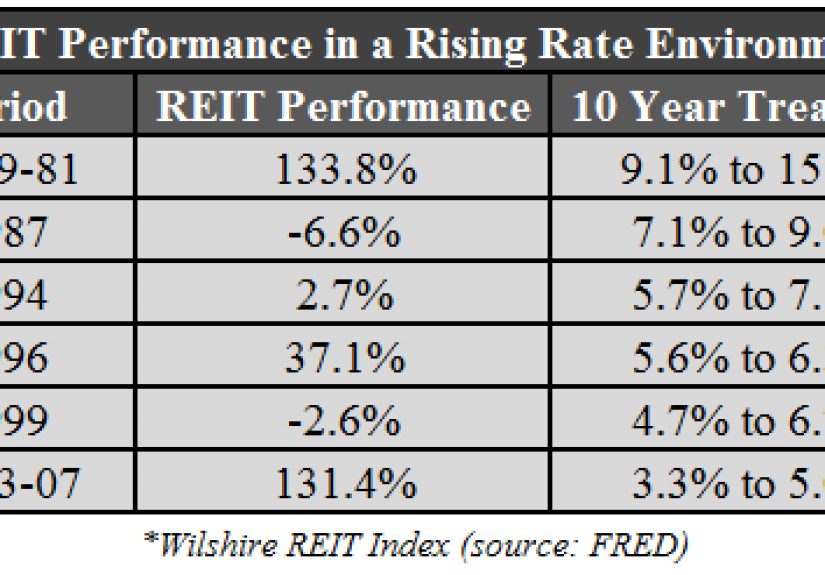

What Recent Market History Says

The last few years gave investors a useful stress test. During the aggressive rate-hike period of 2022 and 2023, real estate valuations, financing conditions, and sentiment all came under pressure. That was the era that helped cement the popular idea that higher rates and REITs simply do not mix.

But the rebound that followed showed why the story cannot end there. Listed REITs posted gains in 2024 after recovering from late-2023 lows, yet performance within the sector was highly uneven. Some subsectors rallied strongly, while others lagged badly. That dispersion is important. It tells investors that balance sheets, property type, and earnings growth can matter more than a broad macro label.

Even so, recent relative performance also reminds us that rate sensitivity is still very real. Real estate underperformed the broader U.S. stock market in 2025, and analysts pointed to interest-rate movements as a major driver. Slower same-store NOI growth also mattered. That combination is a good example of how REIT pricing can struggle when investors do not get enough operating momentum to compensate for an elevated cost of capital.

Commercial real estate conditions have also remained uneven. Some corners of the market have shown stabilization, while refinancing risk continues to loom over borrowers who still need to roll debt in a more expensive funding environment. That matters because public REITs do not operate in a vacuum. They live in the same capital markets ecosystem as the rest of commercial property.

Which REITs Are More Vulnerable When Rates Rise?

- Office-heavy REITs: They face a double headache when financing costs rise and demand remains structurally uncertain.

- Highly leveraged REITs: More debt means less room for error, especially if refinancing is near.

- REITs dependent on external acquisitions: Higher capital costs can freeze growth-by-dealmaking models.

- Mortgage REITs: These can be more sensitive to spread changes, leverage, and funding stress.

- Low-growth property types: If rent growth is weak, there is less operating power available to offset higher rates.

Which REITs May Hold Up Better?

- REITs with strong rent growth: Revenue momentum helps absorb financing pressure.

- REITs with fixed-rate, long-duration debt: These are less exposed to immediate refinancing pain.

- Property sectors with tight supply: Limited new construction can support pricing power.

- Retail formats with healthy fundamentals: Certain retail REITs have entered 2026 with stronger operational support than many investors expected.

- Specialty REITs with differentiated demand drivers: The sector’s performance dispersion has shown that some niches can still shine even when the headline environment looks rough.

What Investors Should Watch Instead of Just Watching the Fed

If you want to evaluate whether rising rates will hurt a specific REIT, skip the lazy one-line take and look at the operating details.

Debt maturity schedule

How much debt comes due in the next one to three years? A manageable maturity ladder is a lot more comforting than a refinancing cliff.

Fixed-rate versus floating-rate exposure

Floating-rate debt transmits rate hikes faster. Fixed-rate debt buys breathing room.

Occupancy and rent growth

Healthy leasing trends can offset higher financing costs. Weak leasing trends cannot.

AFFO payout ratio and dividend coverage

A big yield is nice until it turns out to be held together with duct tape and optimism.

Subsector fundamentals

Supply, tenant demand, and lease structure can overwhelm broad rate narratives.

Management discipline

In a higher-rate world, smart capital allocation matters more. The easy-money era was forgiving. The current environment is not.

So, Will Rising Rates Hurt REIT Performance?

Usually, yes, at least in the short term. Rising rates can pressure valuations, slow acquisition activity, raise refinancing costs, and make REIT dividends less compelling relative to safer income options. That is the basic mechanism, and investors should not ignore it.

But the more useful conclusion is this: rising rates hurt weak REITs more than strong ones, and they hurt some property sectors far more than others. A low-growth, highly leveraged REIT with looming maturities may have a bad time. A well-capitalized REIT with solid occupancy, pricing power, and long-dated fixed-rate debt may do much better than the headline suggests.

That is why serious investors should treat “rates up, REITs down” as a starting point, not a finished analysis. It is a decent shortcut for a market headline. It is a lousy substitute for understanding how real estate businesses actually work.

REIT performance in a rising-rate world is not just about the cost of money. It is about whether the underlying properties can grow cash flow fast enough, consistently enough, and intelligently enough to outrun that higher cost. Some can. Some cannot. That is where the real work begins.

Investor Experiences From a Rising-Rate REIT Cycle

The most common investor experience during a rising-rate cycle is emotional whiplash. A lot of people buy REITs for income and stability, then panic when prices behave like regular stocks. That is exactly what happened when rates surged: investors looked at a portfolio built for yield and suddenly saw sharp price swings instead. The lesson was uncomfortable but valuable. Public REITs may own real estate, but they trade on the stock market, and the market is not known for its calm breathing exercises.

Another frequent experience was learning the hard way that all REITs are not the same. Investors who assumed “real estate is real estate” discovered that an office-focused REIT, a shopping-center REIT, and a specialty REIT could have wildly different outcomes in the same year. Some parts of the market were dragged down by weak demand, refinancing stress, or structural change. Others held up better because rents kept rising, supply stayed tight, or the business model had stronger secular support. That experience pushed many investors away from blanket sector bets and toward more selective analysis.

Income-focused investors also ran into a new kind of comparison problem. When cash and Treasurys started paying more, the old logic of “I need REITs because nothing else yields anything” stopped working. Investors had options again. Some rotated out of REITs entirely. Others stayed in, but became much pickier about dividend safety, payout ratios, and growth potential. In practice, that meant the market started rewarding not just high yields, but believable yields. A giant dividend with shaky coverage became a warning sign instead of a selling point.

There was also a useful experience around patience. Investors who sold on every scary rate headline often missed the point that public REIT prices can overshoot in both directions. Sentiment can get ugly quickly, especially when headlines scream about commercial real estate stress. Yet operating fundamentals do not change at the same speed as daily market mood swings. Investors who kept watching rent growth, occupancy, debt maturities, and balance-sheet quality often ended up with a clearer view than investors who treated every Treasury move like an evacuation order.

Perhaps the most important experience was realizing that a rising-rate period can separate durable REIT businesses from fragile ones. The easy-money environment made a lot of strategies look smarter than they really were. Higher rates exposed who had discipline, who had too much leverage, and who depended too heavily on cheap capital. For investors, that was not fun, but it was useful. It turned a vague macro fear into a practical checklist: Can this REIT refinance safely? Can it grow cash flow? Can it protect the dividend? Can management allocate capital without heroic assumptions? Those questions tend to matter long after the latest Fed headline fades, and they are usually the questions that lead to better decisions.

Conclusion

Rising rates can absolutely hurt REIT performance, but they do not hurt every REIT equally, and they do not hurt for the same reasons every time. Investors who stop at the headline miss the deeper story. The better approach is to examine debt structure, rent growth, property type, and management discipline. In a higher-rate market, REIT investing becomes less about chasing yield and more about understanding business quality. That is not bad news. It is just grown-up investing.