Table of Contents >> Show >> Hide

- What “Working” Should Mean (Because Definitions Matter)

- The Scoreboard: Are Americans Getting Better With Money?

- So… Is Financial Education Working?

- Why “Animal Spirits” Beat Lesson Plans

- The Types of Financial Education That Actually Work Better

- A Practical Playbook: Making Financial Education “Stick” at Home

- What This Means for Schools, Employers, and Policy

- Conclusion: Financial Education WorksBut It Needs Backup

- Real-World Experiences: Where Financial Education Succeeds (and Where It Faceplants)

Financial education is supposed to be the superhero origin story for your money: learn the rules, dodge the traps,

retire on a beach, and only cry tears of joy when you open your credit card statement.

And yet… millions of people can explain compound interest and still get ambushed by a “limited-time offer,” a

sneaky subscription, or a “buy now, pay later” button that might as well whisper, future-you can handle it.

That messy gapbetween what we know and what we dois exactly why the question from Animal Spirits (hosted

on A Wealth of Common Sense) hits a nerve: Is financial education actually working?

Let’s treat this like a real audit. Not a vibes-based “kids these days” rant. We’ll look at what the data says,

why behavior is so stubborn, and what kinds of financial education actually stick in the real worldwhere people

are busy, tired, and one push notification away from buying something called a “hydrating sleep mask” at 1:07 a.m.

What “Working” Should Mean (Because Definitions Matter)

If “financial education” means “I watched a 12-minute video about budgeting once,” then yes, it’s working

beautifully for the video platform.

But if we’re being serious, financial education should be judged like any other intervention:

- Knowledge: Do people understand basic concepts (interest, inflation, risk, diversification)?

- Confidence: Do they feel capable of making decisions without panic-Googling everything?

- Behavior: Do they actually save, pay down high-interest debt, and invest consistently?

- Outcomes: Are they more resilientable to handle emergencies, avoid predatory products, and stay invested?

Most debates get stuck on knowledge. But the scoreboard that matters is behavior and outcomes. You can “know”

vegetables are healthy and still build a diet primarily from drive-thru regret.

The Scoreboard: Are Americans Getting Better With Money?

1) Emergency resilience is improving… but it’s not exactly a victory lap

One of the simplest stress tests is the classic “unexpected $400 expense.” In the Federal Reserve’s annual survey,

63% of adults said they could cover a hypothetical $400 emergency using cash, savings, or a credit

card paid off at the next statement. But 13% said they wouldn’t be able to pay it by any means.

Another benchmark is whether people have a real “rainy day” cushion. In the same report, 55% said

they had set aside money to cover three months of expenses in an emergency fundwhile 30% said they

could not cover three months of expenses by any means.

Translation: a lot of households are doing okay, but a meaningful chunk is one bad week away from a financial

spiral. That’s not a knowledge problem alone. That’s a systems-and-cash-flow problem.

2) Credit cards: the “I understand math” test we keep failing anyway

The FINRA Foundation’s National Financial Capability Study (NFCS) gives a detailed look at behaviorsespecially

the kind that quietly drain wealth (fees, interest, missed payments).

In the latest wave, the share of people who said they always pay their credit cards in full each month fell to

53% (down from 2021). Meanwhile, a majority of credit card holders engaged in at least one behavior

that generates interest or fees, and costly behaviors like paying only the minimum, paying late fees, or using

cash advances show up at uncomfortable rates.

This is the recurring theme: many people understand the “right answer,” but real life keeps handing them the

multiple-choice option that says, “C) Not today.”

3) Confidence is higheven when knowledge is not

Here’s where the “animal spirits” part really shows up. In the NFCS, 64% of adults gave themselves

high marks for financial knowledge, even though quiz performance is much lower on key concepts (like how fast

interest can double debt). In other words: people often feel confident right up until reality sends a pop quiz.

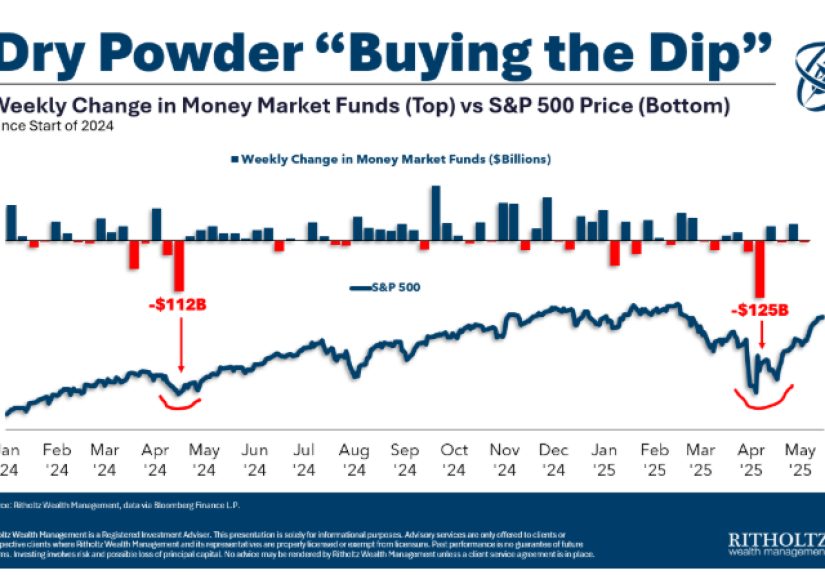

Overconfidence isn’t just a personality quirk; it’s a financial risk factor. It’s how people end up chasing hot

stocks, timing the market, or assuming they’ll “figure it out later” with debt.

4) Overall financial literacy is stuck around “meh”

The TIAA Institute and GFLEC’s Personal Finance (P-Fin) Index has repeatedly found that U.S. adults answer only

about half of its personal finance questions correctly. The latest report puts the overall score at

49%.

That doesn’t mean people are hopeless. It means the baseline is still low enough that small mistakeslike not

understanding interest rates or inflationcan become expensive fast.

So… Is Financial Education Working?

The honest answer is: yes, but not in the way people expect.

If you expect a single class or a one-time workshop to permanently upgrade someone’s money behavior, the evidence

will disappoint you. If you treat financial education as one part of a larger behavior-and-design system, the

evidence gets a lot more encouraging.

What research says when you zoom out

A major meta-analysis from the National Bureau of Economic Research looked at randomized experiments and found

that financial education programs have positive causal effects on financial knowledge and downstream behaviors,

with knowledge effects that are “economically meaningful” and comparable to other educational interventions.

That’s important: it’s not “financial education does nothing.” It’s “financial education helps, but it’s not a

magic wand.” Which is also true for most things that involve humans.

Why results often look smaller in the wild

In real life, people aren’t lab participants. They’re juggling rent, family, healthcare, and the emotional

rollercoaster of checking their accounts when eggs cost what eggs cost now.

Education can move knowledge. Behavior is harder because behavior is crowded out by:

- Cash-flow stress: It’s hard to “budget” when there’s nothing left to budget.

- Friction: Opening an IRA is harder than opening a food delivery app.

- Temptation design: Finance is full of “one-click” decisions that cost money.

- Emotional triggers: Fear and greed don’t care about your spreadsheet.

Why “Animal Spirits” Beat Lesson Plans

The phrase “animal spirits” (popularized in economics as a way to describe human emotion in markets) is a perfect

explanation for why education alone struggles: money decisions are not purely intellectual. They’re emotional,

social, and often made under pressure.

The behavioral traps that show up everywhere

-

Present bias: Future benefits feel abstract; today’s wants feel urgent.

(“I’ll start saving next month” is the financial version of “I’ll start working out Monday.”) - Loss aversion: Losses feel worse than gains feel good, which can cause panic selling.

- Social proof: If everyone is talking about a trade, it feels safereven when it’s not.

- Overconfidence: “I’m above average” is a lovely self-esteem booster and a terrible investing strategy.

Why the environment matters more than your intentions

Modern personal finance is a high-speed obstacle course. Payments are frictionless, credit is easy, and spending

is constantly nudged. The NFCS even notes meaningful adoption of newer tools and behaviors, including

Buy Now Pay Later usage among a sizable share of adults.

Education that doesn’t account for this environment is like teaching someone to swim by showing them a diagram of

water. Helpful, but eventually they still have to get in the pool.

The Types of Financial Education That Actually Work Better

1) “Just-in-time” education beats “someday” education

Teaching investing concepts to someone who won’t invest for five years is like teaching someone parallel parking

in a cornfield. They might remember a few tips, but it won’t stick.

Education works better when it’s tied to a real decision:

- Enrolling in a 401(k) at a new job

- Choosing health insurance during open enrollment

- Picking a repayment plan for student loans

- Deciding whether to carry a credit card balance

2) Action-focused beats information-focused

The Consumer Financial Protection Bureau (CFPB) has emphasized that effective financial education should be

designed to help people achieve financial well-beingnot just memorize terms. That typically means focusing on

behaviors, decision-making, and practical steps instead of trivia.

3) Systems beat willpower

If there’s one “grown-up secret” to money success, it’s this: automation is financial education with a spine.

People who automate saving and investing don’t need daily motivation. They need one good setup day.

- Automatic 401(k) contributions (with automatic increases)

- Automatic transfers to a “rainy day” savings account

- Auto-pay for minimum debt payments to avoid late fees

- Simple investing defaults (like broad diversification and periodic rebalancing)

4) Simplification is a feature, not an insult

The SEC’s investor education materials emphasize fundamentals like asset allocation, diversification, and

rebalancingbecause the basics work, and complexity is often where investors get hurt.

Financial education “works” best when it helps people commit to a simple plan that can survive a bad week, a bad

market, and a bad mood.

A Practical Playbook: Making Financial Education “Stick” at Home

Here’s a simple, realistic framework that turns education into behaviorwithout requiring you to become a

part-time accountant.

Step 1: Build a tiny emergency buffer (start small, win often)

The Fed’s $400 question exists for a reason: emergencies aren’t rare. If your first emergency fund goal feels too

big, shrink it. Start with $200, then $500, then one month. Momentum matters.

Step 2: Kill the most expensive debt first (usually)

If credit card interest is eating your paycheck, investing is like trying to fill a bathtub while the drain is

open. The NFCS shows how common fee-and-interest behaviors are, which is why debt management is often the biggest

“return on effort” move.

Step 3: Automate the boring wins

The goal is to make the “right” decision the default decision. Set contributions, auto-pay what you can, and

reduce the number of times you have to fight yourself.

Step 4: Use one rule to protect yourself from “animal spirits”

Pick a rule you can live with during market chaos. Examples:

- 24-hour rule: No big money moves when you’re emotional.

- Schedule rule: Invest on the same day each month, no matter the headlines.

- Rebalance rule: Adjust allocations on a calendar (not in reaction to news).

Step 5: Track one number weekly

Not a 47-tab spreadsheet. One number. Choose:

- Your checking account “floor” (minimum you want to stay above)

- Your credit card balance trend

- Your savings rate percentage

Behavior change happens when feedback is frequent and simple.

What This Means for Schools, Employers, and Policy

Financial education is often treated like a checkbox. But if we actually want it to work, it needs:

- Clear outcomes: Not “students learned budgeting,” but “students opened a savings account” or “students understood loan terms.”

- Better timing: Teach credit basics before people get credit offers, not after they get debt.

- Rigor and measurement: The U.S. government’s national strategy has warned that growth in financial education hasn’t always come with strong rigor or evaluation.

- Real-world relevance: Include modern products (BNPL, digital payments, high-yield savings, retirement accounts).

- Supports for behavior: Tools, reminders, defaults, and coachingnot just content.

A lot of financial education fails because it’s built like a lecture. It succeeds more often when it’s built like a

system: teach + prompt + simplify + automate.

Conclusion: Financial Education WorksBut It Needs Backup

If financial education is working, it’s working in the same way a gym membership “works.” It helps. It improves

outcomes. It increases the odds. But it doesn’t lift the weights for you.

The data shows real challengespeople juggling emergency expenses, paying interest and fees, and rating their

financial knowledge higher than their quiz performance suggests. At the same time, high-quality research finds

that education can improve knowledge and behavior, especially when it’s targeted and well-designed.

The most practical takeaway from the Animal Spirits question is this:

education alone can’t outmuscle human emotion, marketing, and friction.

But education paired with smart defaults, automation, and “just-in-time” guidance can absolutely move the needle.

So yesfinancial education can work. Just don’t ask it to fight “animal spirits” by itself. Give it a team.

Real-World Experiences: Where Financial Education Succeeds (and Where It Faceplants)

Below are common, real-world patterns people frequently describe in financial coaching, workplace benefits

meetings, and everyday money conversations. They’re not one person’s storythey’re the greatest hits album of

modern personal finance, featuring everyone’s favorite band: “I know what I should do, but…”

Experience #1: The “I’m Good With Money” Credit Card Trap

A common scenario goes like this: someone feels confident because they pay bills on time, have a decent income,

and can explain interest rates. They tell themselves they’re “responsible” with credit. Then a few expensive

months hittravel, holiday spending, a car repair, or medical costs. The balance creeps up. Minimum payments look

manageable, so they keep swiping. A few months later, they’re shocked at how little the balance moves.

This is where education almost worked. They knew interest was bad, but they didn’t have a behavior system:

automatic extra payments, a spending “circuit breaker,” or a planned emergency fund. The fix is usually not more

information. It’s a tiny set of rules: auto-pay to avoid fees, set a weekly balance check, and pick a simple

payoff strategy (like targeting the highest-rate debt first). Once the system exists, knowledge becomes useful

again instead of just… decorative.

Experience #2: The “Market Panic” Lesson Nobody Remembers Until It’s Too Late

Plenty of people can recite investing basics: diversify, think long-term, don’t try to time the market. But when

markets get volatile, the emotional brain shows up with a megaphone. The phone lights up with scary headlines.

Group chats fill with “what are you doing?” messages. Suddenly, the plan feels optional.

The people who hold steady usually have two things: (1) a simple portfolio they understand, and (2) a pre-committed

rule. They rebalance on a schedule. They keep investing monthly. They don’t make big changes on bad-news days.

That’s not just disciplineit’s design. The “education” that sticks is the part that comes with a script for

stressful moments. Without a script, education gets replaced by adrenaline.

Experience #3: The “Financial Class That Helped… Later” Effect

Many people say the most helpful financial education didn’t feel helpful at the time. A high school lesson about

credit didn’t matter until their first credit card offer arrived. A workplace seminar about retirement didn’t

click until they had a 401(k) match in front of them. Education often lands best when it’s tied to an immediate

choice and a clear action.

That’s why “just-in-time” learning wins: a short lesson during open enrollment, a one-page explanation when

choosing a loan, or a quick walkthrough when setting up automatic savings. In those moments, education becomes a

lever people can pull right away. The experience many describe is simple: when education shows up at the exact

moment they need itand makes the next step obviousthey actually use it.

Experience #4: The Quiet Power of One “Boring” Habit

If there’s a single habit that repeatedly shows up in success stories, it’s not “mastering advanced investing.”

It’s consistently savingsometimes in small amountsand increasing it over time. People who build a tiny emergency

fund often describe a surprising side effect: less stress, fewer panic decisions, and fewer “I had to put it on a

card” moments. That cushion buys time and choices.

Financial education helped them understand why the buffer matters. But the buffer happened because they picked a

boring, repeatable behavior: an automatic weekly transfer, a rule to save part of any extra income, or a “floor”

in checking they wouldn’t go below. Education provided the map; a habit provided the transportation.

Put all these experiences together and the theme is clear: financial education works best when it’s paired with

timing (right before real decisions), simplicity (few moving parts), and

systems (automation and rules that protect people from their own “animal spirits”).