Table of Contents >> Show >> Hide

- What “valuation” actually means in the stock market

- Why valuations can look useless during bull markets

- Why valuations still matter a lot

- What the current market says about valuation

- What investors usually get wrong about valuations

- So, do valuations even matter for the stock market?

- Practical takeaways for investors

- Experiences investors often have when valuations stop feeling theoretical

- Conclusion

- SEO Tags

Wall Street loves a dramatic question, and this one has real “are we all just making this up?” energy. When stocks keep rising even though every pundit on television is waving around a price-to-earnings chart like it’s a fire alarm, it’s fair to ask: do valuations even matter for the stock market?

The honest answer is yes. But not in the neat, movie-friendly way most people want. Valuations matter a great deal over the long run, and only occasionally in the short run. They can help explain why future returns may be lower, why some parts of the market look riskier than others, and why bargain-hunting still exists in a world obsessed with mega-cap glamour. What valuations usually cannot do is ring a bell at the top and tell you exactly when the party ends. Markets are rude like that.

If you want the simplest version, here it is: valuation is not a crystal ball. It is more like gravity. A stock market can float above “fair value” for quite a while, especially when earnings are growing, liquidity is plentiful, and investors are convinced a major theme, like artificial intelligence, will rewrite the future. But the higher valuations climb, the harder it becomes for future returns to stay spectacular without near-perfect follow-through.

What “valuation” actually means in the stock market

When investors talk about valuations, they are usually asking a basic question: how much are we paying for a dollar of business performance? That performance can be measured in earnings, sales, book value, cash flow, or some smoothed version of profits over time.

Common valuation metrics

The most familiar metric is the P/E ratio, or price-to-earnings ratio. A company trading at 20 times earnings is more expensive than one trading at 10 times earnings, assuming the quality and growth outlook are similar. Then there is the forward P/E, which uses expected future earnings instead of trailing ones. Investors also watch the Shiller CAPE, which smooths earnings over 10 years to reduce the distortion caused by recessions and booms.

None of these numbers is perfect. A fast-growing company may deserve a higher multiple. A cyclical company may look cheap right before profits collapse. And an index can appear expensive because a handful of giant firms are doing most of the heavy lifting. That last point matters a lot today, because market concentration can make “the market” look richer than the average stock inside it.

Why valuations can look useless during bull markets

This is the part that frustrates disciplined investors. Expensive markets can stay expensive. Very expensive markets can get even more expensive. And sometimes the crowd screaming “bubble” winds up looking early, which is financially indistinguishable from looking wrong.

That happens because stock prices are not set by valuation alone. In the short run, they are also driven by earnings revisions, interest rates, economic growth, sentiment, policy shifts, and plain old narrative power. If investors believe profits will compound rapidly for years, they may happily pay up today. If central banks are easing, recession fears are fading, or a new technology story captures the imagination, multiples can stretch far beyond historical norms.

The late-1990s dot-com era is still the classic cautionary tale. Valuations were clearly extreme well before the bubble burst, but that did not stop the market from climbing first. More recently, the AI-led run in U.S. mega-cap stocks showed how a small group of companies can dominate returns even while the broader market looks less exciting under the hood. In that kind of environment, valuation skeptics often feel like they brought a calculator to a laser show.

So when people say valuations do not matter, what they usually mean is this: expensive markets do not always fall right away. That is true. It is also not the same thing as valuations being irrelevant.

Why valuations still matter a lot

Here is where the joke turns serious. Valuations are not especially reliable as a 12-month timing tool, but they become much more useful over longer horizons. Over five, seven, or 10 years, the price you pay has a much stronger relationship with the return you are likely to earn.

Think of it this way. If you buy a wonderful business or a broad stock index at a sky-high multiple, one of two things has to happen for you to get excellent future returns. Either earnings must explode higher and justify that premium, or investors must become willing to pay an even sillier price later. That second option can work for a while. It just is not a comfortable retirement plan.

This is why many long-term capital market forecasts are now relatively muted for U.S. stocks. Several major firms expect U.S. equities to deliver positive returns over the coming decade, but not the kind of easy double-digit gains investors grew used to over the strongest parts of the post-2009 bull market. In other words, valuations matter because they shape the starting point. And starting point math is annoyingly stubborn.

Valuation affects expected return, not just risk

One common misunderstanding is that valuations only tell you whether something is “dangerous.” In reality, they say a lot about expected return. An expensive market can still move higher, but its margin for error is thinner. A cheaper market may feel less glamorous, yet offer better odds for patient investors because lower starting prices leave more room for upside.

This is where valuations become genuinely useful. They help investors form realistic expectations. If the market is richly priced, it may still deserve a place in a portfolio, but it probably does not deserve blind faith, heroic forecasts, or a dramatic over-allocation born from FOMO.

What the current market says about valuation

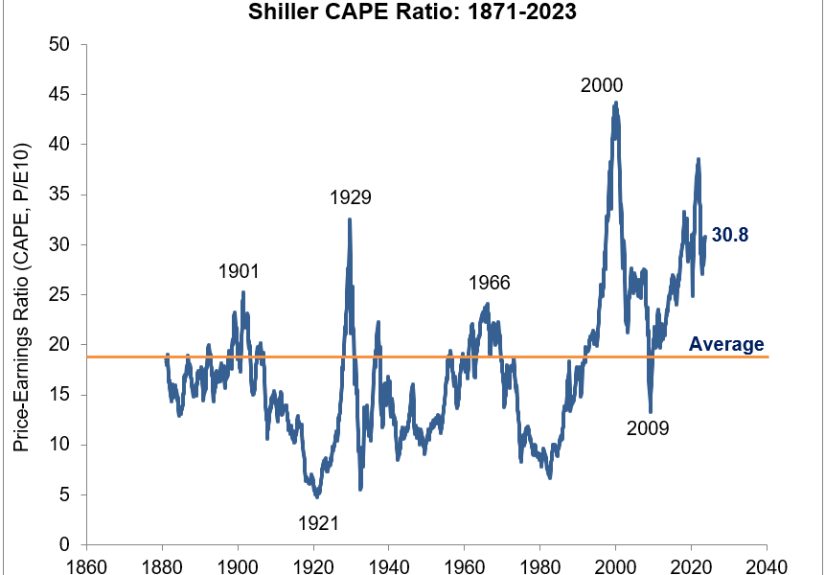

As of early April 2026, broad U.S. valuation gauges still looked elevated by historical standards. The S&P 500’s Shiller CAPE was near 39, more than double its long-run mean near 17. That does not guarantee an imminent collapse. It does suggest that the market is priced for a lot of good news already.

That idea shows up in multiple ways. Some long-term forecast models now imply more modest U.S. equity returns over the next decade than many investors might expect after recent market strength. Morningstar’s fair-value framework has also pointed to a U.S. market that is not dirt-cheap, with more attractive pricing in areas like small-cap stocks and value stocks. In plain English, the entire market is not equally expensive. The priciest parts tend to be the most celebrated parts.

That distinction matters. When investors say “the market is expensive,” they often mean a narrow slice of giant growth companies is very expensive. The average stock may be more reasonably valued. Concentration can distort the big-picture story, which is why digging beyond the headline index is so important.

Where value may still exist

If valuations matter, then the next logical question is where the bargains are hiding. Lately, the most common answers have included U.S. small caps, value stocks, and some international markets. These areas may not win the popularity contest, but they often look more attractive on traditional valuation measures.

That does not mean they will outperform next Tuesday. It means their starting prices may offer better long-run odds. Investors who only chase what has already worked often wind up buying a wonderful story at a terrible price. That is a fun hobby in fashion. It is less charming in portfolio construction.

What investors usually get wrong about valuations

Mistake No. 1: Treating valuation like a countdown clock

A high multiple does not tell you when the market will fall. It only tells you the market is more vulnerable if growth slows, rates stay higher, or investors become less willing to pay premium prices. Valuation is a condition, not a schedule.

Mistake No. 2: Ignoring earnings entirely

A stock can look expensive and still be worth owning if earnings keep compounding. Great businesses often look “too expensive” for years. The trick is distinguishing between a high-quality company with genuine profit power and a market darling priced like it already solved capitalism.

Mistake No. 3: Assuming expensive means “sell everything”

That move sounds bold and usually ages poorly. Rich valuations may argue for better diversification, more selective buying, and lower return expectations. They do not automatically argue for abandoning stocks altogether. Investors who wait endlessly for the perfect entry point often miss more upside than they avoid downside.

Mistake No. 4: Forgetting the market is not one giant stock

The S&P 500 can be pricey while parts of the market are merely fair, and some niches may even be cheap. Sector composition, index concentration, and style leadership all influence the valuation story. Looking only at one headline number can leave you both informed and misled, which is a very Wall Street outcome.

So, do valuations even matter for the stock market?

Absolutely. They matter because they influence expected returns, frame risk, and help explain why some market segments deserve caution while others deserve curiosity. They matter because paying 40 times normalized earnings is simply different from paying 15 times, even if both assets have the same ticker-symbol charisma. And they matter because the stock market is not just a scoreboard of excitement; eventually, it is also a weighing machine for cash flows, profits, and the price investors paid to access them.

But valuations do not matter in the magical way many people want. They are not a reliable alarm clock for the next correction. They cannot tell you the exact month a rally will end. They do not invalidate strong businesses, and they do not remove the need to understand earnings, balance sheets, and macro conditions.

The smarter view is this: valuations matter most when setting expectations, not when trying to win a market-timing contest. They tell you whether future returns are being pulled forward, whether risk is hiding behind optimism, and whether the easiest money may already have been made. That is not sexy. It is just useful. And in investing, useful beats sexy more often than social media would have you believe.

Practical takeaways for investors

If you are a long-term investor, the lesson is not to panic when valuations look high. The lesson is to stop assuming high past returns automatically lead to high future returns. Consider broad diversification. Rebalance instead of making dramatic all-or-nothing moves. Watch how much of your portfolio is concentrated in the same names, themes, and valuation profile. And if you are adding new money, pay attention to price rather than buying whatever has the brightest spotlight.

In short, valuations matter the way nutrition matters. You may not feel the effect after one meal, but over time the pattern shows up. Markets can binge on enthusiasm for longer than expected. Eventually, though, math sits down at the table.

Experiences investors often have when valuations stop feeling theoretical

If you have ever lived through an expensive market, you know the experience is not neat or academic. It is emotional, weirdly social, and full of moments that make sensible people question their own judgment. High valuations do not arrive wearing a name tag that says, “Hello, I am future return compression.” They usually arrive disguised as confidence, momentum, and stories that sound incredibly persuasive after a big run higher.

One common experience is watching the market keep climbing after you already decided it was too expensive. That can be maddening. You start by feeling prudent, then patient, then slightly annoyed, and finally like the only person at the party who keeps asking what the bill will be. Meanwhile, stocks rise, headlines celebrate innovation, and people who bought aggressively begin to sound like prophets. Expensive markets have a way of making discipline feel old-fashioned.

Another experience is discovering that “the market” and your portfolio are not behaving the same way at all. The index may be marching higher because a handful of giant stocks are carrying it, while many other names do very little. That creates a strange psychological split. On paper, the market looks unstoppable. In real life, plenty of investors feel like they are jogging behind a parade float driven by seven companies and an army of semiconductors. This is where valuation discussions become more personal. You are no longer debating theory; you are deciding whether to chase concentration, stick to diversification, or accept the pain of lagging for a while.

Then comes the experience of the first real wobble. Maybe it is a weak earnings report, a rate scare, a geopolitical shock, or a sudden shift in narrative. Nothing has to break completely. Richly valued markets just need a reason to become less adored. When that happens, investors often realize that expensive assets do not simply drift lower in a polite, orderly fashion. They can reprice fast because the premium was built on confidence, and confidence is not exactly famous for its emotional stability.

There is also a quieter experience that long-term investors recognize: realizing that valuation does not need to predict next quarter to still be helpful. Maybe you did not sell the top. Maybe you did not buy the exact bottom. But paying attention to valuation nudged you to diversify more, rebalance sooner, and lower your assumptions before the crowd did. That does not make for exciting cocktail-party storytelling. It does, however, make for better investing behavior.

In that sense, the real experience of valuation is not dramatic market prophecy. It is the slow development of judgment. You stop asking, “When will this overpriced market crash?” and start asking better questions: “What am I being asked to believe at this price? How much perfection is already baked in? What could go right, and what has to go right?” Once investors start thinking that way, valuations become less like a scary headline and more like a useful filter. They may not predict every twist in the stock market, but they can save you from confusing excitement with value. And that, over a lifetime of investing, matters more than one perfectly timed call ever could.

Conclusion

So yes, valuations matter for the stock market. They matter most as a guide to future return potential, portfolio risk, and where real opportunity may still exist when headline indexes look stretched. They do not work like a stopwatch, and they will not spare you from every bull-market headache. But they remain one of the most useful reality checks investors have. In a market that regularly falls in love with its own reflection, valuations are the friend willing to say, “You look great, but let’s not get carried away.”