Table of Contents >> Show >> Hide

- What Does “Fixed Income Has Income Again” Mean?

- Why Bond Yields Are Higher Now

- The Big Shift: Bonds Are Competing Again

- Where Investors Are Finding Income

- Understanding the Main Risks

- Why Duration Deserves Respect Again

- How Fixed Income Fits Into a Portfolio

- A Practical Example: Building a Simple Income Strategy

- What Investors Should Avoid

- Experiences and Lessons From the Return of Fixed-Income Income

- Conclusion: Income Is Back, but Selectivity Still Matters

For years, fixed income felt like the financial equivalent of ordering decaf coffee: technically useful, but not exactly thrilling. Investors bought bonds for stability, diversification, and a modest stream of payments, while quietly accepting that the “income” part of fixed income had become more of a polite suggestion than a reality. Then interest rates rose, inflation refused to retire quietly, and suddenly bonds started doing something they had not done in a long time: paying investors meaningful income.

That is the simple but powerful idea behind today’s bond market: fixed income has income again. U.S. Treasury yields, investment-grade corporate bonds, certificates of deposit, municipal bonds, and high-quality bond funds now offer yields that can matter inside a portfolio. This does not mean bonds are risk-free. It does not mean every bond is a bargain. And it certainly does not mean investors should sprint into the highest-yielding product they can find like it is the last slice of pizza at a party. But it does mean the asset class deserves a fresh look.

In 2026, the Federal Reserve’s policy rate remains well above the near-zero levels that shaped much of the post-2008 investing era. Inflation is still a central concern, and Treasury yields have stayed elevated enough to make bonds competitive again. For retirees, savers, income-focused investors, and even long-term growth investors who want ballast in a portfolio, fixed income is no longer the boring corner of the room. It is still wearing sensible shoes, but now it brought snacks.

What Does “Fixed Income Has Income Again” Mean?

Fixed income refers to investments that typically make scheduled interest payments and return principal at maturity, assuming the issuer remains financially healthy. Common examples include U.S. Treasury securities, corporate bonds, municipal bonds, agency mortgage-backed securities, bond mutual funds, bond ETFs, and CDs.

The phrase “fixed income has income again” means that starting yields are high enough to offer investors a real cash-flow opportunity. After many years when high-quality bonds often produced very low yields, investors can now find more attractive income without automatically reaching into the riskiest corners of the market.

Starting yield matters because it is one of the strongest indicators of a bond investor’s future return potential over time. A bond purchased with a 4% or 5% yield gives the investor a larger income cushion than a bond purchased at 1% or 2%. That cushion can help absorb some price volatility if rates move higher. It can also make bonds more useful for investors who need regular income from their portfolios.

Why Bond Yields Are Higher Now

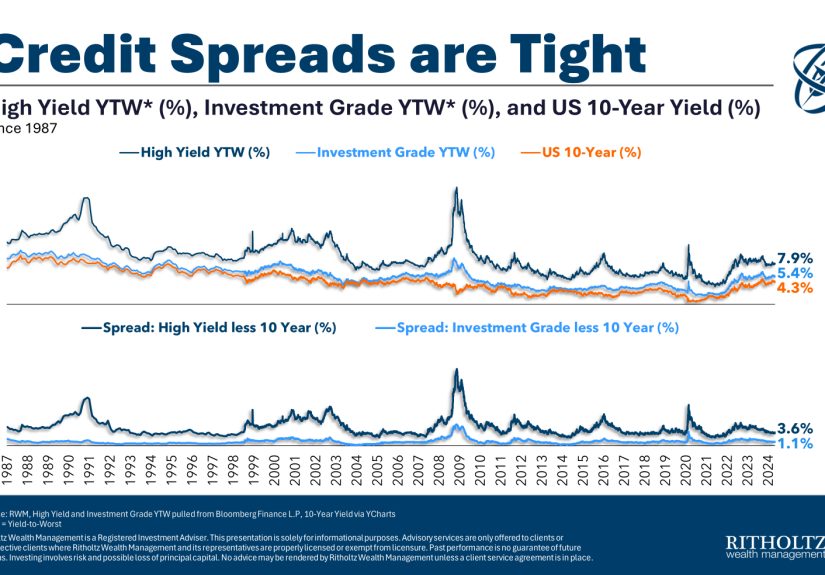

Bond yields rose because the economic environment changed. Inflation surged earlier in the decade, and the Federal Reserve responded by lifting short-term interest rates aggressively. Even after rate cuts from peak levels, policy rates remain much higher than the ultra-low-rate world many investors grew used to.

When interest rates rise, newly issued bonds must offer higher coupons to attract buyers. Older bonds with lower coupons usually fall in price so their yields become more competitive. That price decline was painful for investors who owned bonds before rates rose, especially long-duration bonds. But for new money, reinvested coupons, and portfolios gradually rolling into higher-yielding securities, the picture is much better.

Inflation is another reason yields remain elevated. Investors demand compensation for the possibility that future dollars may buy less. If inflation runs at 3% to 4%, a 1% bond yield looks like a very bad joke. A 4% to 6% yield, depending on bond type and credit quality, starts to look more reasonable.

The Big Shift: Bonds Are Competing Again

For much of the low-rate era, investors faced an uncomfortable choice: accept tiny yields from safer bonds or take more risk in stocks, real estate, private credit, or high-yield debt. That pushed many investors farther out on the risk spectrum. The famous acronym TINA“there is no alternative”was often used to describe why stocks looked attractive even at high valuations.

Today, there is an alternative. High-quality fixed income can provide income, diversification, and potential downside protection. This does not make bonds automatically superior to stocks. Stocks still offer long-term growth potential that bonds generally cannot match. But when a Treasury, CD, or investment-grade bond fund offers meaningful yield, investors can be more selective. They do not have to chase every hot stock trend or pretend that volatility is a personality trait.

Where Investors Are Finding Income

1. U.S. Treasury Securities

U.S. Treasuries are backed by the full faith and credit of the U.S. government, making them one of the highest-quality fixed-income options. Treasury bills, notes, and bonds offer different maturities, from a few weeks to 30 years. Short-term Treasury bills can appeal to investors who want liquidity and income, while intermediate-term Treasuries may offer a better balance between yield and interest-rate sensitivity.

Long-term Treasuries can provide more price appreciation if yields fall, but they also carry more duration risk. In plain English: they can move around a lot. A long Treasury bond may be safe from default risk, but it is not safe from market price swings.

2. Investment-Grade Corporate Bonds

Investment-grade corporate bonds are issued by financially stronger companies. They usually pay more than Treasuries because investors take on credit risk. That extra yield is called a spread. When the economy is stable and corporate balance sheets are healthy, investment-grade bonds can offer attractive income without venturing too far into risky territory.

The key is quality. Not all corporate bonds are created equal. A bond issued by a large, profitable company with steady cash flow is very different from one issued by a highly indebted company hoping everything goes perfectly. Hope, as investors learn sooner or later, is not a credit strategy.

3. Municipal Bonds

Municipal bonds are issued by states, cities, counties, and other public entities. Their interest is often exempt from federal income tax and may also be exempt from state and local taxes for residents of the issuing state. That makes municipal bonds especially interesting for investors in higher tax brackets.

When comparing municipal bonds with taxable bonds, investors should use tax-equivalent yield. A muni yielding 3.5% may be worth more than a taxable bond yielding 5% for some investors after taxes. The math depends on the investor’s tax bracket, location, and whether the bond is subject to alternative minimum tax.

4. Certificates of Deposit and High-Quality Cash Alternatives

CDs and high-yield savings products have also benefited from higher rates. They are not exactly the same as bonds, but they compete for the same conservative dollars. CDs can be useful for short-term goals, emergency reserves, or investors who want predictable income and FDIC insurance within applicable limits.

The trade-off is reinvestment risk. A short-term CD may pay well today, but when it matures, rates could be lower. Investors who keep everything short term may feel safe, but they may also miss the chance to lock in attractive yields for longer.

5. Bond Funds and ETFs

Bond mutual funds and ETFs provide diversification and professional management. They can hold hundreds or thousands of bonds, making them easier to use than building a bond ladder one security at a time. Funds also provide liquidity, although their prices fluctuate daily.

Investors should pay attention to duration, credit quality, expense ratios, and the fund’s role in the portfolio. A short-term Treasury ETF is not the same thing as a high-yield corporate bond fund. Both may live under the “fixed income” umbrella, but one is a raincoat and the other is a trampoline.

Understanding the Main Risks

Interest-Rate Risk

Bond prices and interest rates generally move in opposite directions. If rates rise, existing bond prices usually fall. The longer the bond’s duration, the more sensitive it is to rate changes. This is why long-term bond funds suffered when rates rose sharply.

However, higher starting yields can help. If a bond fund yields 5%, that income can offset some price declines over time. This is one reason today’s fixed-income market looks healthier than it did when yields were near historic lows.

Credit Risk

Credit risk is the chance that a bond issuer fails to make interest or principal payments. Treasuries have minimal default risk, while corporate bonds, municipal bonds, and high-yield bonds vary widely. Higher yield often means higher risk. Sometimes it means investors are being paid well for taking risk. Other times it means the market is waving a red flag while wearing a neon vest.

Inflation Risk

Inflation reduces the purchasing power of fixed payments. If a bond pays 4% but inflation is 4%, the real return before taxes is not especially exciting. Treasury Inflation-Protected Securities, or TIPS, can help address this risk because their principal adjusts with inflation. Still, TIPS prices can fluctuate, and they are not magic shields against every market condition.

Reinvestment Risk

Reinvestment risk occurs when income or maturing bonds must be reinvested at lower rates. This is especially important for investors holding only short-term bonds or CDs. If rates fall, today’s attractive income could disappear quickly. A balanced maturity strategy can help manage this risk.

Why Duration Deserves Respect Again

Duration is a measure of a bond’s sensitivity to interest-rate changes. Short-duration bonds are less sensitive, while long-duration bonds are more sensitive. During the rate-hiking cycle, many investors learned about duration the hard way. It was the financial equivalent of discovering that the stove is hot by placing both hands on it.

Now that yields are higher, duration can be more useful. If rates fall, intermediate and longer-duration bonds may gain in price. If rates stay elevated, investors may still collect meaningful income. The sweet spot for many investors may be intermediate duration, where income is attractive but interest-rate risk is not as extreme as it is at the long end of the curve.

How Fixed Income Fits Into a Portfolio

Fixed income can serve several roles. It can generate income, reduce portfolio volatility, preserve capital, and provide liquidity. For retirees, bonds may help fund spending needs. For younger investors, bonds can stabilize a stock-heavy portfolio and create dry powder for future opportunities.

A classic balanced portfolio might include stocks for growth and bonds for stability. The exact allocation depends on age, risk tolerance, goals, time horizon, tax situation, and income needs. A 30-year-old saving for retirement may use bonds differently than a 68-year-old drawing portfolio income. The right bond strategy is not a universal recipe; it is more like tailoring a suit. The sleeves matter.

A Practical Example: Building a Simple Income Strategy

Imagine an investor with $100,000 set aside for conservative income. Instead of placing all of it in a savings account, the investor might divide it into several buckets:

- 25% in Treasury bills or a money market fund for liquidity

- 30% in short-term bonds or CDs for near-term income

- 30% in intermediate-term Treasury or investment-grade bond funds

- 15% in municipal bonds or TIPS, depending on tax and inflation concerns

This is not a recommendation, but it shows how investors can combine liquidity, income, and diversification. The goal is not to grab the highest possible yield. The goal is to create a durable income plan that does not collapse the moment markets get moody.

What Investors Should Avoid

The return of income can tempt investors into bad habits. One common mistake is chasing yield without understanding risk. A bond yielding 9% may look attractive, but the yield may reflect real concerns about default, liquidity, or credit quality. Another mistake is assuming cash is always safest. Cash is stable in nominal terms, but it can lose purchasing power to inflation and may face reinvestment risk if rates decline.

Investors should also avoid overconcentration. Owning one or two individual corporate bonds can expose a portfolio to company-specific problems. Diversified funds or carefully built ladders can reduce that risk. Finally, investors should avoid ignoring taxes. The after-tax return is what actually reaches the investor’s pocket, and pockets are famously where money prefers to end up.

Experiences and Lessons From the Return of Fixed-Income Income

The comeback of fixed-income income has changed the way many investors think about portfolio construction. During the low-rate years, conversations about bonds often sounded apologetic. Advisors would explain that bonds were still useful for diversification, even though the income was tiny. Investors nodded politely, then asked whether they should buy more growth stocks, dividend stocks, or real estate investment trusts to make up the difference.

Today, the conversation feels different. Investors who once ignored bonds are asking serious questions about Treasury ladders, municipal bond funds, investment-grade corporates, and how to lock in yields before rates fall. Retirees who depended heavily on stock dividends can now compare those dividends with bond yields that may be more predictable. Conservative savers who spent years earning almost nothing on cash can finally see meaningful interest payments again.

One common experience is psychological relief. Income investors like seeing actual cash flow. A bond coupon may not be glamorous, but it arrives with a certain quiet dignity. It does not need a product launch, a viral app, or a CEO wearing a black turtleneck. It simply pays, assuming the issuer remains sound. That predictability can be comforting, especially when stock markets are volatile.

Another lesson is that higher yield does not eliminate the need for discipline. Many investors learned in 2022 and 2023 that bonds can lose value when rates rise quickly. That experience was painful, but useful. It reminded investors that “safe” and “stable” are not always the same thing. A Treasury bond may be safe from default, but a long-term Treasury fund can still decline sharply if yields jump. This is why matching bond duration to time horizon matters.

Some investors have also rediscovered bond ladders. A ladder spreads maturities across different dates, allowing part of the portfolio to mature regularly. This can provide liquidity and reduce the pressure to guess the perfect interest-rate move. When one rung matures, the investor can spend the money or reinvest it at current rates. It is not flashy, but neither is flossing, and dentists keep insisting that works too.

For people approaching retirement, the return of income can support more flexible planning. Instead of relying only on selling shares during market downturns, retirees may use bond interest, CD maturities, and Treasury payments to fund part of their spending. This can reduce sequence-of-returns risk, which is the danger of taking withdrawals from a portfolio after market losses early in retirement.

Younger investors can benefit too. Higher bond yields make portfolio diversification more rewarding. A young investor may still hold a stock-heavy allocation, but a modest bond position can now contribute income instead of simply acting as a volatility cushion. That income can be reinvested, helping compound returns over time.

The biggest experience-based takeaway is simple: fixed income works best when it has a job. Before buying any bond or bond fund, investors should ask what role it serves. Is it for emergency liquidity? Retirement income? Tax-efficient cash flow? Inflation protection? Portfolio stability? Each goal points to a different solution. When bonds are chosen with purpose, they can be powerful. When they are chosen only because the yield looks shiny, trouble may be waiting behind the curtain.

Conclusion: Income Is Back, but Selectivity Still Matters

Fixed income has income again, and that is good news for investors who value cash flow, diversification, and portfolio balance. Higher starting yields have restored much of the appeal that bonds lost during the low-rate era. Treasuries, municipal bonds, investment-grade corporates, CDs, and diversified bond funds can now play meaningful roles in income strategies.

Still, investors should stay thoughtful. Interest-rate risk, credit risk, inflation risk, and reinvestment risk have not disappeared. The best fixed-income strategy is not the one with the highest yield; it is the one that fits the investor’s goals, time horizon, tax situation, and tolerance for volatility.

In other words, bonds are back at the table. They may not dance on the table like speculative stocks, but they do bring something very useful: income, structure, and a calmer voice when markets start yelling.

Note: This article is for educational and editorial purposes only and should not be treated as personalized investment, tax, or financial advice. Investors should review their own situation or consult a qualified financial professional before making investment decisions.