Table of Contents >> Show >> Hide

- Why People Think the Stock Market Is Rigged

- The Stock Market Is Not a Perfect Level Playing Field

- Retail Investors Have More Access Than Ever

- Regulation Exists for a Reason

- Low Costs Changed the Game for Small Investors

- Most Professionals Struggle to Beat the Market Too

- What “Rigged” Gets Wrong About Market Losses

- The Real Risks Small Investors Should Watch

- How the Little Guy Can Compete Intelligently

- Specific Example: The Index Investor vs. the Hype Chaser

- Experience Section: Lessons From Real-World Investing Behavior

- Conclusion: The Market Is Challenging, Not Rigged

Every time the stock market drops, jumps, twists, or behaves like a caffeinated squirrel on a power line, someone declares that the whole thing is “rigged against the little guy.” It is an understandable reaction. When billion-dollar hedge funds have supercomputers, Wall Street firms have armies of analysts, and regular investors have a phone app, a lunch break, and maybe a suspiciously confident YouTube video, the playing field can look uneven.

But uneven is not the same as rigged. The U.S. stock market is complex, competitive, imperfect, highly regulated, and occasionally ridiculous. It is not a magical money machine, and it is not a casino secretly designed to vaporize every retail investor’s paycheck. For the average person, the biggest obstacles are usually not hidden Wall Street traps. They are high-risk speculation, emotional decision-making, poor diversification, excessive trading, chasing hype, and misunderstanding how long-term investing works.

The truth is more encouraging: the little guy has more access, lower costs, better tools, broader diversification options, and stronger investor protections than at almost any point in market history. That does not mean every investor wins. It means the game is not automatically stacked against ordinary people who invest patiently, intelligently, and with realistic expectations.

Why People Think the Stock Market Is Rigged

Let’s be honest: the “rigged market” idea did not come from nowhere. Retail investors have watched meme stocks soar and crash, brokerages restrict certain trades during extreme volatility, insiders get investigated for suspicious timing, and high-frequency traders move faster than a human thumb can tap “buy.” Add in confusing jargon like payment for order flow, dark pools, market makers, bid-ask spreads, and short selling, and suddenly the stock market sounds less like investing and more like a secret club where the password is “adjusted EBITDA.”

There are also real scandals. Pump-and-dump schemes exist. Fraud exists. Insider trading cases happen. Some financial products are too expensive, too complicated, or too aggressively sold. None of that should be brushed aside. A healthy market needs skepticism, regulators, transparency, enforcement, and investors who read more than the headline.

However, the existence of fraud does not prove that the entire stock market is rigged. By that logic, because some restaurants fail health inspections, every sandwich is a conspiracy. The better conclusion is this: bad actors exist, but the market itself has rules, surveillance, disclosures, competition, and enforcement systems designed to protect investors and punish manipulation.

The Stock Market Is Not a Perfect Level Playing Field

One reason the “rigged” argument feels persuasive is that big institutions do have advantages. They may have faster data, better research teams, sophisticated risk systems, and access to private market opportunities that regular investors do not. They can negotiate lower trading costs, hire experts, and build complex strategies across stocks, bonds, options, futures, currencies, and derivatives.

But here is the twist: most regular investors do not need to beat Wall Street at Wall Street’s own game. You do not need a server next to an exchange, a PhD in applied mathematics, or a Bloomberg terminal glowing in your living room like a sacred altar. If your goal is long-term wealth building, you can benefit from broad market growth through low-cost index funds, ETFs, retirement accounts, dollar-cost averaging, and diversification.

Professional traders compete in milliseconds. Long-term investors compete in decades. Those are different sports. A hedge fund may be trying to scalp pennies on a trade. A household investor may be trying to build retirement savings over 25 years. The first is Formula 1. The second is planting an oak tree. Both involve movement, but only one requires wearing a fireproof suit.

Retail Investors Have More Access Than Ever

For much of financial history, small investors faced meaningful barriers: high commissions, high mutual fund fees, minimum investment requirements, limited research access, and slow execution. Today, many mainstream brokerages offer commission-free online stock and ETF trades, fractional shares, no account minimums, educational tools, retirement calculators, and automatic investing features.

That matters. A person no longer needs thousands of dollars to buy one share of an expensive company or build a diversified portfolio. Fractional shares allow investors to buy based on a dollar amount. Low-cost ETFs make it possible to own exposure to hundreds or thousands of companies with a single trade. Target-date funds can package diversification and rebalancing into one retirement-friendly option.

In other words, the little guy has tools that previous generations would have considered financial science fiction. Your grandfather may have had to call a broker, pay a fat commission, and wait. You can research a fund, compare fees, read disclosures, and invest a small amount before your coffee gets cold. Whether that is wise depends on what you buy, of course. Technology gives access; judgment still has to drive the car.

Regulation Exists for a Reason

The U.S. market is regulated by agencies and self-regulatory organizations that oversee exchanges, brokers, market makers, investment advisers, public companies, and trading behavior. The Securities and Exchange Commission requires public companies to disclose financial information. FINRA supervises broker-dealers and enforces rules around sales practices, communications, and order handling. SIPC helps restore missing customer assets if a member brokerage firm fails financially, although it does not protect investors from normal market losses.

Best-execution rules are especially important. Brokers are expected to seek favorable execution terms for customer orders. Payment for order flow, where a broker receives compensation for routing orders to a market maker, is controversial because it can create conflicts. But it is not legal permission to ignore customers. Regulators have repeatedly emphasized that payment arrangements cannot override best-execution obligations.

Recent updates to order execution disclosure rules have also aimed to improve transparency around execution quality, including information relevant to odd-lot and fractional-share orders. Translation: regulators know the plumbing matters, and they keep updating the pipes. Is the plumbing glamorous? No. But neither is your home’s plumbing, and you notice very quickly when it stops working.

Low Costs Changed the Game for Small Investors

One of the strongest arguments against “the market is rigged” is the dramatic decline in investing costs. Fund fees have fallen substantially over the past two decades, and low-cost index funds have become mainstream. This is a huge advantage for ordinary investors because fees compound in reverse: every extra dollar paid in expenses is a dollar that cannot grow for you.

Consider the difference between paying 1.00% annually and paying 0.05% annually on a diversified fund. That gap may look tiny, like a rounding error wearing loafers. But over 20 or 30 years, it can add up to thousands or even tens of thousands of dollars depending on account size and returns. Cost control is one of the few investing factors an individual can actually control.

This is where the little guy has a real edge. Institutions may have advanced strategies, but regular investors can choose simple, low-cost funds and avoid paying for complexity they do not need. A boring portfolio with broad diversification and low fees may not impress anyone at a dinner party, but it has historically been a powerful wealth-building tool. Besides, most dinner party stock tips age like unrefrigerated shrimp.

Most Professionals Struggle to Beat the Market Too

If the market were truly rigged in favor of professionals, most professional stock pickers would consistently crush the indexes. Yet long-running performance studies show that many active managers underperform their benchmarks over time. In recent SPIVA data, a large share of active large-cap U.S. equity funds lagged the S&P 500, reinforcing a familiar lesson: beating the market is hard even when investing is your full-time job.

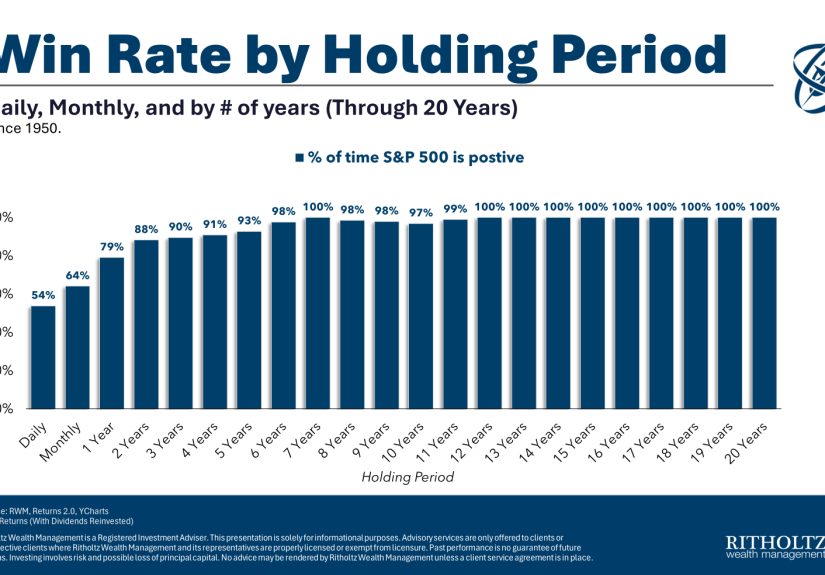

This should be oddly comforting. The average investor does not have to outsmart every hedge fund manager. They can simply own the market through diversified index funds and let capitalism do its messy, innovative, occasionally dramatic thing. Companies compete, profits grow, productivity improves, and shareholders participate in that growth over time.

That does not mean indexes always go up. They can fall sharply. Bear markets hurt. Recessions are real. Inflation, interest rates, wars, bubbles, and policy changes can all shake portfolios. But volatility is not proof of rigging. It is the price investors pay for the possibility of higher long-term returns.

What “Rigged” Gets Wrong About Market Losses

Many investors call the market rigged after buying a hot stock near the top and watching it collapse. That pain is real. But a bad outcome does not always mean an unfair process. Sometimes the issue is overvaluation. Sometimes it is poor research. Sometimes it is concentration risk. Sometimes it is buying because strangers online used rocket emojis with dangerous confidence.

The stock market does not know your purchase price, your rent payment, or your emotional attachment to a ticker symbol. It is an auction driven by expectations, liquidity, earnings, interest rates, sentiment, and risk. Prices move because buyers and sellers constantly disagree. That disagreement is not evidence of a trap. It is the market doing market things.

Retail investors often hurt themselves by confusing trading with investing. Trading asks, “Can I buy this now and sell it soon for more?” Investing asks, “Can I own a sensible piece of productive assets over time?” The first can work, but it is difficult and usually tax-inefficient. The second is less exciting, but it tends to be more realistic for households building wealth.

The Real Risks Small Investors Should Watch

1. Overconcentration

Owning one or two stocks can feel thrilling when they rise. It feels less thrilling when earnings disappoint and your portfolio falls like a dropped lasagna. Diversification spreads risk across companies, sectors, and sometimes asset classes. It does not eliminate losses, but it can reduce the damage from any single company’s bad news.

2. Chasing Hype

Markets love stories. Artificial intelligence, electric vehicles, crypto-adjacent stocks, biotech breakthroughs, and turnaround plays can all produce excitement. Some stories become real businesses. Others become cautionary tales with nicer logos. Buying only because “everyone is talking about it” is not analysis; it is financial karaoke.

3. Panic Selling

Long-term investors often lose not because the market is rigged, but because they abandon their plan at the worst possible moment. Selling after a large decline may feel safe, but it can lock in losses and cause investors to miss recoveries. A written investment plan can help reduce emotional decision-making when headlines start shouting.

4. Ignoring Fees and Taxes

Fees, spreads, expense ratios, advisory costs, and taxes may seem small individually. Together, they can quietly nibble at returns like a mouse with a 401(k). Tax-efficient accounts, low-cost funds, and lower turnover can help investors keep more of what they earn.

5. Confusing Fraud With Volatility

Fraud involves deception. Volatility involves price movement. They are not the same. A stock falling 40% is not automatically fraud. A promoter guaranteeing huge returns, pressuring you to act immediately, or claiming secret insider access is a much louder warning sign.

How the Little Guy Can Compete Intelligently

The best way for ordinary investors to compete is not to become miniature hedge funds. It is to build a process that uses the advantages available to them: patience, low costs, diversification, tax-advantaged accounts, consistent contributions, and a refusal to panic every time the market gets dramatic.

A practical approach might include maintaining an emergency fund before investing aggressively, using workplace retirement plans when available, considering diversified index funds or ETFs, reinvesting dividends, reviewing asset allocation periodically, and avoiding money needed in the near term for risky stock investments. None of this sounds like a blockbuster movie. That is fine. Good investing is often boring because boring is easier to repeat.

Dollar-cost averaging can also help investors avoid the impossible task of perfectly timing the market. By investing a set amount on a regular schedule, investors buy more shares when prices are lower and fewer when prices are higher. It does not guarantee profits or prevent losses, but it can reduce the emotional pressure of deciding whether today is “the perfect day” to invest. Spoiler: the perfect day is usually visible only in hindsight, where everyone is a genius and no one admits they panic-sold.

Specific Example: The Index Investor vs. the Hype Chaser

Imagine two investors, both starting with modest savings. Investor A buys a diversified, low-cost total market fund every month and rarely checks the account. Investor B jumps between trending stocks, sells after drops, buys after viral posts, and treats earnings calls like sporting events. Investor B may occasionally have spectacular wins. But Investor A has a repeatable system that does not require predicting next week’s market mood.

Over long periods, consistency can be more powerful than brilliance. The market rewards ownership of productive assets, but it does not reward impatience on command. A small investor who avoids major mistakes may outperform a smarter investor who cannot control behavior. Investing is one of the few arenas where doing less can sometimes produce better results. Try telling that to someone assembling furniture without instructions.

Experience Section: Lessons From Real-World Investing Behavior

One of the clearest experiences related to this topic is watching how ordinary investors react during market stress. When the market is calm, everyone believes they are long-term investors. When the market falls 20%, many suddenly become short-term philosophers with sweaty palms. The lesson is simple: risk tolerance is not what you say in a bull market; it is what you can actually live with during a sell-off.

Small investors often feel disadvantaged because they see big institutions moving markets in the news. But in everyday investing, the greatest advantage a regular person has is the ability to ignore short-term noise. A pension fund, hedge fund, or portfolio manager may be judged every quarter. A household investor saving for retirement may have decades. That longer time horizon can be an enormous edge if the investor uses it properly.

Another common experience is the temptation to “wait for a better entry point.” Many people delay investing because they think the market is too high, too uncertain, too political, too expensive, or too weird. Sometimes they are right for a while. But waiting can become a habit, and missed compounding is expensive. A disciplined schedule can help remove some of that hesitation.

Investors also learn, sometimes painfully, that simplicity is underrated. A portfolio with dozens of overlapping funds, speculative stocks, options trades, and hot themes may look sophisticated. But sophistication is not the same as strength. A simpler portfolio is easier to understand, rebalance, and stick with. If you cannot explain what you own and why you own it, your portfolio may be wearing a fake mustache.

There is also an emotional lesson: the market does not care about fairness in the way people do. Good companies can fall. Bad companies can rally. Great news can already be priced in. A stock can drop after “beating earnings” because expectations were even higher. This can feel unfair, but it is not rigging. It is the constant adjustment of expectations.

Many small investors become better once they stop trying to win every trade. They focus instead on avoiding financial self-sabotage: no panic selling, no all-in bets, no borrowing money to chase a stock, no buying purely because of social media hype, and no confusing a temporary win with a permanent skill upgrade. The market has a funny way of humbling people who mistake luck for genius.

The most useful experience is this: small investors do not need special treatment to succeed. They need fair access, low costs, reliable information, investor protections, and good habits. The modern market provides many of those tools. The habits are still up to the investor.

Conclusion: The Market Is Challenging, Not Rigged

No, the stock market is not rigged against the little guy. It is challenging, noisy, competitive, and sometimes brutally humbling. It contains conflicts, loopholes, scams, and sophisticated players. But it also offers ordinary investors unprecedented access to diversified investments, low fees, fractional shares, retirement accounts, regulatory protections, educational resources, and decades of evidence supporting disciplined long-term participation.

The little guy loses most often not because Wall Street flips a secret switch, but because impatience, concentration, hype, fear, and high costs quietly do the damage. The good news is that these are manageable risks. A retail investor who keeps costs low, diversifies broadly, invests consistently, avoids obvious scams, and thinks in years rather than minutes is not powerless. In fact, that investor may be using the market exactly as it is best used.

The stock market is not a guaranteed path to wealth, and no article should pretend otherwise. But it is also not a locked vault reserved for insiders. For the little guy, the door is open. The trick is not running through it blindfolded while holding a meme stock and a dream.