Table of Contents >> Show >> Hide

- The Two Main Engines of Stock Market Returns

- Dividends and Buybacks Still Matter

- Interest Rates: The Market’s Strictest Chaperone

- Inflation: Not Just a Grocery Store Problem

- Economic Growth and the Business Cycle

- Market Concentration and the Giant-Stock Effect

- Technology, Productivity, and the AI Narrative

- Sentiment, Liquidity, and Good Old-Fashioned Human Emotion

- What’s Driving the Stock Market Returns Right Now?

- What Investors Should Watch Next

- Investor Experiences: What This Feels Like in Real Life

- Conclusion

The stock market loves to act mysterious, like a magician who refuses to reveal how the rabbit got into the hat. One day stocks soar because the economy looks strong. The next day they drop because the economy looks too strong and investors worry interest rates will stay higher for longer. It can feel ridiculous, dramatic, and oddly theatrical. But under all the noise, stock market returns are not random confetti. They are driven by a handful of forces that show up again and again: earnings growth, valuation changes, dividends and buybacks, interest rates, inflation, economic growth, and investor psychology.

If you want to understand what’s driving the stock market returns, you do not need a crystal ball or an emotional support spreadsheet. You need a framework. Once you understand how profits, rates, sentiment, and market concentration interact, the market starts to look less like chaos and more like a machine with several noisy moving parts.

In plain American English, here is what is really powering stock market returns and why the answer is usually “a little bit of everything, but not equally.”

The Two Main Engines of Stock Market Returns

At the highest level, stock market returns come from two big engines. The first is business performance. When companies grow revenue, protect margins, generate cash, and increase earnings over time, their stocks tend to rise with them. The second is what investors are willing to pay for those earnings. That is valuation. A company can post decent profits, but if investors suddenly decide the stock is overpriced, the return can still be weak. On the flip side, a company can have only modest improvement in profits and still deliver strong returns if investors become more optimistic and bid up the valuation multiple.

That is why market returns are never just about whether businesses are “doing well.” They are also about whether expectations are rising or falling. The market is a discounting machine. It constantly tries to price tomorrow before tomorrow has the decency to arrive.

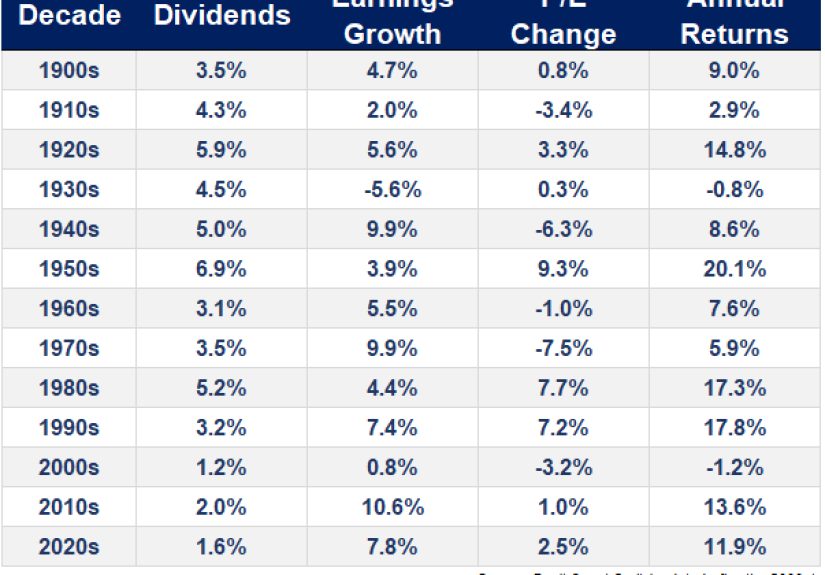

Earnings Growth: The Fundamental Fuel

Earnings are the most durable driver of long-term stock returns. In the end, stocks represent ownership in businesses, and businesses that earn more money over time tend to create more value. If corporate profits rise steadily, the market usually has a solid foundation for gains. This is why earnings season matters so much. It is not just a parade of executives using phrases like “headwinds” and “disciplined execution.” It is the market checking whether the profit engine is still humming.

When earnings growth is broad and healthy, returns tend to be more durable. When earnings growth is concentrated in only a few sectors or companies, the market can still rise, but that rise becomes more fragile. It starts leaning on a smaller number of winners, and that can make the overall market more sensitive to disappointment.

Valuation Expansion and Contraction

Valuation is where stock market returns get spicy. Investors often talk about the price-to-earnings ratio, or P/E ratio, because it captures how much the market is willing to pay for a dollar of earnings. If a company earns more and its P/E stays the same, the stock usually rises in a fairly rational way. But if the P/E expands, meaning investors become willing to pay a higher multiple for the same earnings stream, returns can accelerate. That is multiple expansion.

Of course, the reverse also happens. If valuations get too rich, future returns can become harder to earn. Stocks may keep rising for a while, but the math gets less forgiving. Investors are essentially pulling future optimism into today’s price. That can work beautifully until it does not, which is Wall Street’s favorite plot twist.

This is one reason why a great year for the market can actually lower future return expectations. Strong price gains driven mostly by richer valuations often make the next chapter less generous. It is wonderful at the party and awkward the morning after.

Dividends and Buybacks Still Matter

When people talk about stock market returns, they often focus only on price appreciation. That is like judging a pizza by the box. Total return also includes dividends and, increasingly, share buybacks. Dividends provide direct cash to shareholders. In flat or choppy markets, that cash return can make a meaningful difference. Over long stretches, reinvested dividends have historically played a major role in wealth creation.

Buybacks matter because they reduce the number of shares outstanding. If a company repurchases stock at sensible valuations, the remaining shareholders own a slightly larger piece of the business. Earnings per share can improve even if the company’s total profit growth is not explosive. Buybacks are not magic, and they can be wasteful when done at inflated prices, but they are absolutely part of the modern U.S. market return story.

In many corners of the market, shareholder return is now a blend of dividends, buybacks, and capital discipline. Companies that generate strong free cash flow and know what to do with it tend to earn more investor trust than companies that burn cash while promising the moon, Mars, and possibly a robot butler.

Interest Rates: The Market’s Strictest Chaperone

If earnings are the fuel, interest rates are often the thermostat. Rates influence stock market returns in several ways. First, they affect borrowing costs. Higher rates can squeeze profit margins, especially for businesses with meaningful debt or capital needs. Second, rates change how investors value future cash flows. When rates rise, future earnings are discounted more heavily, which tends to hurt richly valued growth stocks the most. Third, higher bond yields create competition for stocks. If investors can earn more from safer assets, stocks need to work harder to justify their prices.

That is why markets obsess over the Federal Reserve. Stocks do not merely react to the level of rates; they react to the path, the pace, and the surprise factor. A market that is prepared for higher rates can sometimes absorb them. A market that is caught leaning the wrong way can throw a full theatrical faint.

It is also important to remember that not all rate increases mean the same thing. If rates rise because growth is improving and corporate profits are strengthening, stocks may hold up reasonably well. If rates rise because inflation is sticky or policy is turning more restrictive, the damage can be larger. The market is always asking the same question in different outfits: “Why are rates moving?”

Inflation: Not Just a Grocery Store Problem

Inflation drives stock market returns because it reshapes both profits and valuations. When inflation rises, some businesses can pass higher costs on to customers. Others cannot. That creates winners and losers. Companies with pricing power, efficient operations, and strong brands often handle inflation better than firms with thin margins and weak customer loyalty.

Inflation also matters because it influences interest rates and real yields. Even modest inflation surprises can reset expectations for monetary policy, and that can ripple through the entire market. Growth stocks may wobble. Small caps may struggle with financing costs. Defensive sectors may suddenly look attractive. In other words, inflation is not just an economics headline. It is a return driver because it affects how much future profit is worth right now.

Markets do not merely care whether inflation is high or low. They care whether inflation is higher or lower than expected. Surprise is often the real villain. Investors can live with many things, but they hate being startled before coffee.

Economic Growth and the Business Cycle

The stock market and the economy are related, but they are not twins. They are more like cousins who show up to the same family reunion wearing very different outfits. Strong economic growth can support higher revenues, better employment, healthier consumer demand, and stronger business investment. That generally helps corporate profits and, by extension, stock returns.

But markets are forward-looking. They often move before the economy does. Stocks may rally while economic data still looks weak because investors expect improvement ahead. Or stocks may fall while recent economic data still looks fine because investors see trouble coming. That disconnect confuses people every cycle.

Even so, economic growth still matters. Consumer spending, capital expenditure, housing activity, credit conditions, and labor market strength all shape the earnings backdrop. If the economy is expanding at a healthy pace without overheating, that is often a friendly setup for equities. If growth slows sharply, companies may face weaker demand and thinner margins. If growth is too hot, the market may worry that rate cuts will vanish like fries at a family dinner.

Market Concentration and the Giant-Stock Effect

One of the most important recent drivers of stock market returns has been concentration. In a market-cap-weighted index like the S&P 500, the largest companies have the biggest influence. When a handful of mega-cap stocks deliver outsized gains, they can drag the whole index higher even if many smaller stocks are doing very little.

This matters because it changes how investors interpret “the market.” A strong index return may not mean broad strength across hundreds of companies. It may mean a select group of dominant businesses is driving most of the action. That can happen when those companies have stronger earnings growth, better margins, superior balance sheets, and a compelling long-term narrative, such as artificial intelligence, cloud computing, or digital infrastructure.

Concentration can be great while it works. It can also increase risk. If returns depend too heavily on a small group of leaders, disappointment in just a few names can shake the entire index. That is why investors watch signs of market broadening so closely. Broad participation tends to make a bull market look healthier. Narrow leadership can still be profitable, but it is less comforting once the music gets weird.

Technology, Productivity, and the AI Narrative

Innovation has always been a driver of stock market returns, but certain waves of innovation hit harder than others. In recent years, the AI buildout and broader productivity story have shaped market leadership. Investors are trying to figure out which companies will gain pricing power, margin expansion, and durable growth from new technologies, and which companies are simply wearing the AI label like a rented tuxedo.

The reason technology narratives move markets is simple: investors pay up for the possibility of future earnings acceleration. If a company is seen as a real beneficiary of a technological shift, its valuation can expand long before the full earnings payoff arrives. That can generate strong returns fast. But it also raises the bar. Once a stock is priced for brilliance, it must keep being brilliant.

That is why the recent market story has not just been “technology is good.” It has been “technology is good, but only when profits, cash flow, and execution can support the excitement.” When markets start demanding proof instead of PowerPoint, the difference between hype and durable return drivers becomes very clear.

Sentiment, Liquidity, and Good Old-Fashioned Human Emotion

Not every stock market move can be explained by spreadsheets alone. Sentiment matters. Liquidity matters. Positioning matters. When investors are optimistic, cash moves into risk assets, valuation multiples rise, and market breadth can improve. When fear takes over, even strong companies can get dragged lower because investors sell what they can, not just what they should.

Liquidity is especially important. Markets tend to perform better when financial conditions are supportive, credit is available, and investors feel comfortable taking risk. When liquidity tightens, valuations usually come under pressure. The market starts caring much more about balance sheet strength, free cash flow, and whether a company can fund growth without begging the capital markets for a fresh allowance.

This is why the stock market can sometimes look irrational in the short run. It is not purely a scorecard for current profits. It is a live auction driven by expectations, fear, greed, policy signals, and thousands of people convincing themselves that this time they are definitely being logical.

What’s Driving the Stock Market Returns Right Now?

Lately, the return picture has been a mix of still-important mega-cap leadership, AI-linked optimism, resilient corporate earnings, and ongoing debate about how restrictive interest rates remain. Investors have also been balancing two truths at the same time: first, that strong businesses can keep delivering returns even in a tougher rate environment; and second, that elevated valuations leave less room for error.

That combination creates a more selective market. Companies with genuine earnings power, durable margins, and strong cash generation tend to be rewarded. Companies that depend mostly on narrative, leverage, or heroic assumptions face a tougher audience. In other words, the market is still willing to clap, but it wants to see the trick done properly.

Another emerging driver is broadening participation. If returns start spreading beyond the largest technology names into industrials, financials, energy, healthcare, and select small-cap or value areas, the market’s foundation can look stronger. If leadership narrows again, investors may keep making money, but the ride could remain bumpier than anyone would prefer.

What Investors Should Watch Next

If you want to understand the next phase of stock market returns, watch a few simple things. Start with earnings revisions. Are analysts raising or cutting profit expectations? Next, watch valuations. Are investors paying more for each dollar of earnings, or are multiples compressing? Then watch inflation and rates. Are price pressures easing enough to support friendlier financial conditions, or do higher real yields keep acting like a brick in the backpack?

Also pay attention to breadth. Are more stocks participating in gains, or is the index leaning on a small number of giants? Finally, watch cash flow quality. In a world where money is not free, companies that can self-fund growth tend to look much more attractive than businesses that survive mainly on hope and aggressive adjectives.

The market rarely sends a single clean signal. It usually sends five signals at once, then changes its mind during lunch. But if you follow earnings, valuations, rates, inflation, and breadth, you will understand most of what actually drives returns.

Investor Experiences: What This Feels Like in Real Life

Here is the part investors rarely admit out loud: understanding what drives stock market returns is emotionally harder than it is intellectually. On paper, the framework is straightforward. Earnings matter. Valuations matter. Rates matter. Inflation matters. In real life, however, investors experience the market as a series of temptations, doubts, and sudden bursts of false genius.

In a rising market, it is easy to believe returns are being driven by your insight rather than by a friendly tide lifting nearly every decent boat. People start saying things like, “I had conviction,” when what they really had was a strong index and a smartphone. That is part of the investor experience. Bull markets flatter us. They make complicated outcomes look obvious in hindsight and convince ordinary people that buying one popular stock was an act of strategic brilliance worthy of a documentary.

Then the mood shifts. A hot inflation report lands. Bond yields jump. A few market leaders wobble. Suddenly everyone discovers the words “valuation risk” as if they invented them in their garage over the weekend. Investors who ignored price multiples during the rally begin discussing discounted cash flows with the urgency of emergency room doctors. That is another real experience tied to stock market returns: the same facts feel either boring or terrifying depending on what prices did this week.

Long-term investors also learn that returns rarely arrive in a neat, emotionally satisfying sequence. You might buy a strong company with healthy earnings, shareholder-friendly capital returns, and a reasonable valuation, only to watch it go nowhere for months. Meanwhile, a wildly expensive stock with a louder story can sprint ahead. This is where experience matters. The market does not pay people for being right immediately. It pays people when fundamentals and expectations eventually meet in the same room.

There is also the strange experience of living through concentration. When only a handful of giant stocks are driving index gains, investors can feel both invested and left behind at the same time. Their portfolio statement may be green, yet they still feel as if they missed the real party because they did not own enough of the market’s favorite names. That gap between portfolio reality and psychological satisfaction is one of the most underappreciated parts of investing.

Over time, many investors discover that the most valuable experience is not predicting every market move. It is learning how not to overreact when the drivers of return temporarily change. Sometimes earnings lead. Sometimes falling yields boost valuations. Sometimes dividends and buybacks quietly do the heavy lifting while headlines scream about something else. Sometimes the best-performing stocks are boring businesses with great cash flow, and sometimes they are linked to the biggest innovation story on the planet.

The experienced investor learns to ask better questions instead of chasing louder answers. Is profit growth real? Is the valuation still defendable? Are rates helping or hurting? Is the market broadening or narrowing? Is this move based on improving fundamentals or just collective excitement wearing expensive shoes?

That perspective does not remove volatility. It simply makes volatility easier to survive. And in the stock market, survival matters because the compounding only works for people who manage to stay in the game long enough to enjoy it.

Conclusion

So, what’s driving the stock market returns? The honest answer is a combination of company earnings, dividends, buybacks, valuation multiples, interest rates, inflation, economic growth, market concentration, and investor sentiment. Over the long run, fundamentals usually win. Over shorter stretches, valuation changes and policy expectations can dominate. In modern markets, concentration and innovation narratives can amplify both gains and risks.

The smartest way to think about stock market returns is not as one big mystery, but as a layered equation. First, ask whether businesses are creating more profit and cash flow. Then ask what price investors are willing to pay for that progress. Then add the macro backdrop, especially inflation and rates. Finally, layer in sentiment, liquidity, and whether gains are broad or narrow.

Once you see those pieces clearly, the market stops looking like random madness and starts looking like what it really is: a fast-moving debate about future profits, future prices, and how much optimism investors can responsibly stuff into one trading day.